Recent Search

Popular Searches

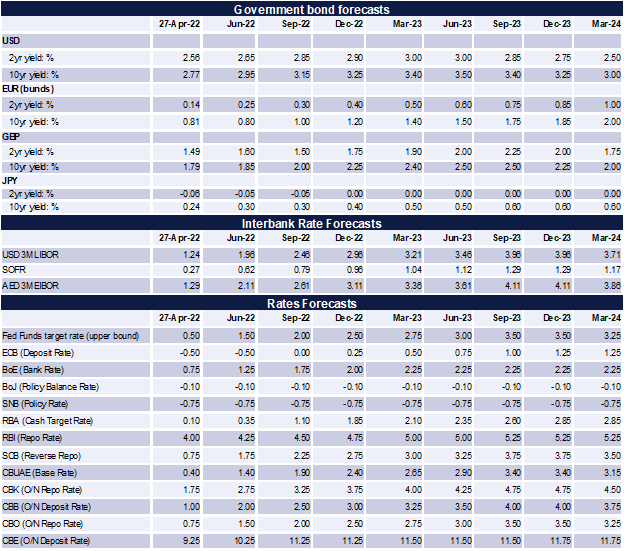

We expect that the Federal Reserve will raise rates by 50bps at the May FOMC meeting, taking the Fed Funds rate to 1% on the upper bound. Several Fed speakers, including Fed chair Jerome Powell, have spoken vocally about the need to combat historically high inflation in the US with rates needing to get above neutral levels ‘expeditiously.’ Should that new mantra hold among Fed policymakers, swapping out for the ‘transitory’ narrative that held in 2021, we expect that the Fed will follow in June with another 50bps hike and at least 100bps of more hikes by the end of the year. That will bring the Fed Funds rate at the end of 2022 to 2.5%, up from our previous expectation of 2%. In addition to higher rates, the Fed will also start to run down its balance sheet at a monthly pace of USD 95bn, helping to tighten liquidity conditions further.

The imperative to get inflation under control is clear. Headline CPI rose to 8.5% y/y in March as high energy and food costs push prices higher and while core CPI did slow its pace of growth, it is nevertheless at elevated levels of 6.5%. Wage growth will also remain a headwind for investment with average hourly earnings up by 5.6% in March and even if inflation slows, prices will still be high and may prompt workers to keep seeking higher incomes.

Inflation expectations are also showing no sign of easing. The 5y5y inflation expectation rate from the St. Louis Fed is at around 2.6%, its highest level since 2014 and well above the Fed’s 2% target level for moderate price growth. Real yields on US Treasuries have moved up close to neutral levels, helping to propel nominal USTs higher with the 10yr yield within reach of 3% for the first time since 2018.

Risks for rates tilted to upside

The risks for rates this year appear skewed to the upside given the hawkish tilt of the Fed at present and the uncertainty on the inflation outlook. James Bullard, president of the St Louis Fed, is open to as much as a 75bps hike at the May meeting while Powell himself indicated that the market was “appropriately” pricing in as many as four 50bps hikes this year.

Our expectation at the start of the year was that commodity price pressures would fade over the course of 2022 but with Russia’s war in Ukraine looking entrenched, the risks for energy and food costs also appear to be for higher rather than substantially lower prices. Fed policy can do little to affect the exogenous variables of sanctions on Russian exports of energy products but can impact domestic demand by making consumer activity that much more expensive. The challenge for the Fed is what level of economic slowdown they are willing to accept in order to tame inflation.

At present it does appear that the Fed is ready to accept rates considerably above neutral, even if it comes at the expense of the labour market and broader economic activity. We are sceptical that a soft-landing or moderate slowdown in the economy can be achieved and in our view the dampening effects of much tighter monetary policy on the economy will be much more apparent in 2023 than in this year.

The hawkish tone from the Fed will keep upward pressure on the short end of the UST curve and we expect yields to keep rising from their current levels, at least over the rest of 2022 and into the first half of 2023. While the ECB has also now shifted toward dealing with inflation as a more serious threat to the eurozone economy, we expect that yield differentials will still favour the dollar over the Euro this year. The BoJ remains an outlier among developed market central banks in keeping policy so accommodative, helping to push USDJPY substantially higher.

Source: Emirates NBD Research

Source: Emirates NBD Research