Recent Search

Popular Searches

The FOMC meets this week, just two days after the US election on November 5th. Our ex-ante assumption is that the Fed will follow its initial 50bps cut to the Fed Funds rate in September with another 25bps and look through the political developments that will follow the election and continue with a stance of making policy less restrictive.

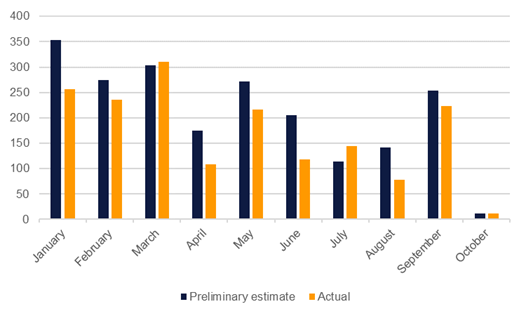

Markets were fairly steady in October in expecting that the Fed would cut at the November FOMC, with a quarter point move the more likely outcome as a string of positive economic data in September helped to dampen expectations for a second consecutive 50bps cut. The prospect of a move this week, regardless of the outcome of the election, seems to have been set more firmly following the release of the October non-farm payrolls report which disappointed sharply on the downside. Just 12,000 jobs were added last month with all the gains coming from the public sector. There was bound to be a disappointing print for October as parts of the US endured destructive hurricanes and strike activity meant manufacturing employment dropped sharply.

Source: BLS, Emirates NBD Research.

Source: BLS, Emirates NBD Research.

While the October print has been impacted by these one-off variables and markets may ultimately discount it, downward revisions to the prior two months data suggest an underlying cooling of activity in the labour market. Employment data has only been revised higher for two months this year and by a far smaller degree than downward revisions.

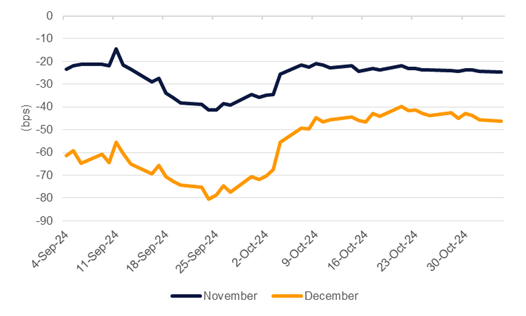

Where the Fed goes after the November meeting is still a little less certain. A day ahead of the US election markets are pricing in 46bps of cuts by the December 18 FOMC meeting or about an 86% chance of an additional 25bps cut. That’s up from a 74% chance only one week ago as markets respond to the weak October non-farm payrolls. Market pricing for the rest of 2025 will harden once it becomes clear what kind of fiscal and trade policies will be introduced under a new administration with markets swinging between a near maintenance of the status quo under Vice President Kamala Harris or a higher inflationary environment under former President Donald Trump.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

Edward Bell

Edward Bell