Recent Search

Popular Searches

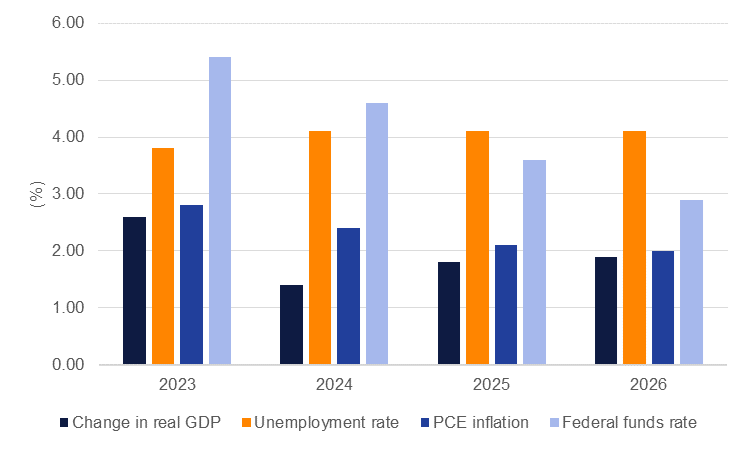

The Federal Reserve kept the Fed Funds rate at 5.5% on the upper bound at its December meeting. The Fed noted that “economic activity has slowed” in recent data while “job gains…remain strong.” The only other change to the Fed’s statement was to water down the prospect of further rate hikes by tweaking the language to “any additional policy firming” from “additional policy firming” in its prior statement. In its summary of economic projections the Fed revised up its GDP growth forecast for 2023 to 2.6% from 2.1% previously and marginally reduced its outlook for 2024 to 1.4% from 1.5% in the September SEP. The Fed also cut its forecast for inflation, expecting PCE inflation at 2.8% for this year, down from more than 3% previously, and sliding to 2.4% in 2024, still ahead of target, before easing to the 2% target level by end of 2025. Headline PCE inflation was at 3% in its most recent print for October.

Source: Federal Reserve, Emirates NBD Research

Source: Federal Reserve, Emirates NBD Research

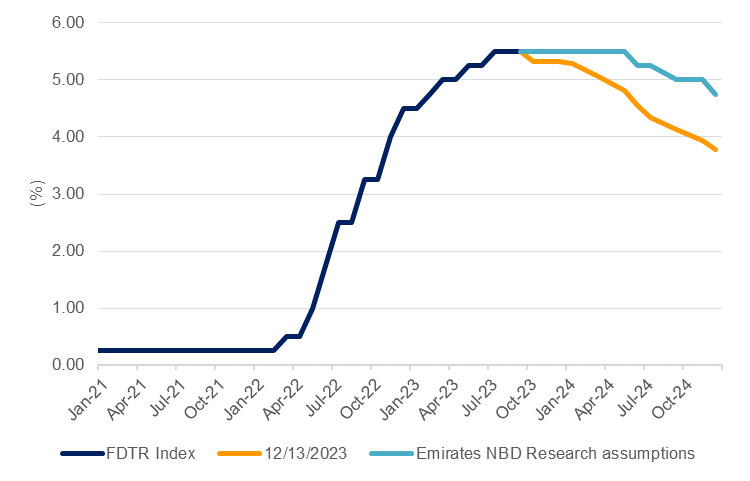

In its outlook for rates, the dots plot implied three 25bps cuts from current levels to take the Fed Funds rate to 4.75% on the upper bound by the end of 2024, in line with our own expectations. Fed chair Jerome Powell said that Fed was “aware of the risk” in keeping policy too tight for too long and that the Fed didn’t need to wait until inflation returned to 2% before it began cutting rates. Unlike its prior dots plot, no policy maker sees the need for rates to go higher with the one dot at 6.125% removed entirely. Overall the December FOMC is in line with our view that the Fed will be less aggressive on easing than markets are currently implying but that they will nevertheless begin cutting rates next year. Our call for rate cuts to begin midway through 2024 and then proceed on a quarterly sequential basis remains intact provided there is no material deterioration in economic conditions. Upside risk to our rates call (more rate cuts) would be based on a faster easing in inflation, particularly in core services inflation. That could potentially mean a rate cut as early as Q1 next year.

Markets interpreted the December FOMC as a dovish stance given the Fed outlined three cuts to policy rates for 2024, compared with two previously, and from a lower terminal level . Yields on the front end of the curve tumbled with the 2yr UST down 30bps at the close to settle at 4.4265% while the 10yr settled lower by 18bps to 4.0164% and it is extending its move to below 4% in early trade today, its lowest level since July 2023. The dollar sold off sharply against peer currencies overnight in response to the more dovish rates expectations from Fed policy makers.

Futures and options markets have aggressively repriced rate cuts for next year after slashing their expectations following the stronger than expected nonfarm payrolls for November. The chance of a first cut in March has a nearly 90% probability according to market pricing with further cuts to follow over the rest of the year to six in total. That scale of easing still looks too aggressive compared with projections for economic activity to slow but not collapse in 2024.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

Edward Bell

Edward Bell