Recent Search

Popular Searches

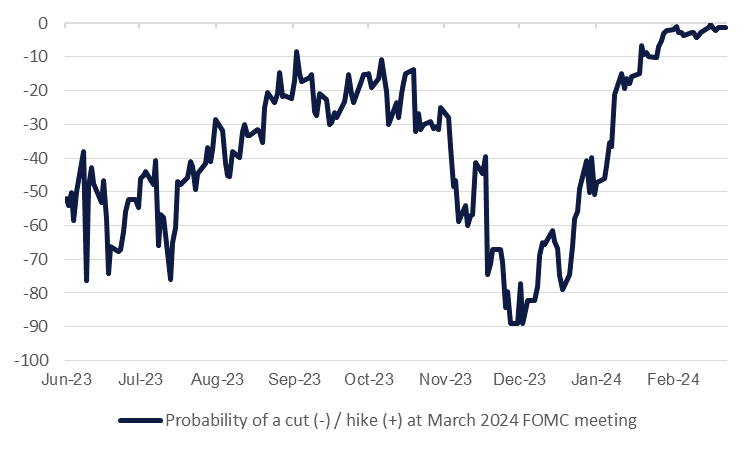

The FOMC sets policy this week with their two-day meeting ending on March 20th. We expect the Fed Funds target rate to remain at 5.5% on the upper bound, unchanged since July 2023 when the Fed last hiked by 25bps. Markets are likewise no longer pricing in a cut in policy rates at the March meeting though expectations have shifted substantially since the end of 2023 when overnight swaps markets were pricing a 90% probability of a cut in March.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

Several hotter than expected inflation prints for the US, along with further signs of labour market strength, have helped to shift market expectations for rates to move lower only later in 2024 while commentary from Fed officials, including Chair Jerome Powell has stressed that they need to have confidence that inflation is heading lower on a sustained basis before they would feel comfortable with cutting rates. This has reinforced our view that the Fed will be patient in adjusting policy downward and we still expect three 25bps cuts this year starting from the June FOMC meeting and proceeding on a sequential quarterly basis.

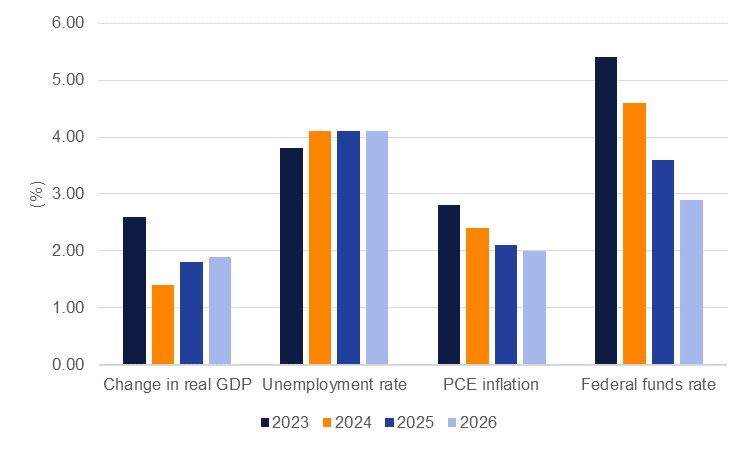

More focus this week will likely fall on the Fed’s revised Summary of Economic Projections, their first for this year. When they last published their economic expectations in December 2023 the Fed expected PCE inflation to cool to 2.4% from 2.8%, the unemployment rate to pick up slightly and for a substantial slowdown in growth – all consistent with a “soft landing” for the US economy. On rates, the median of the Fed’s dots plot was for 75bps of rate cuts in 2024 before rates were nudged lower over the next several years to a terminal rate of 2.5%.

Source: Federal Reserve, Emirates NBD Research.

Source: Federal Reserve, Emirates NBD Research.

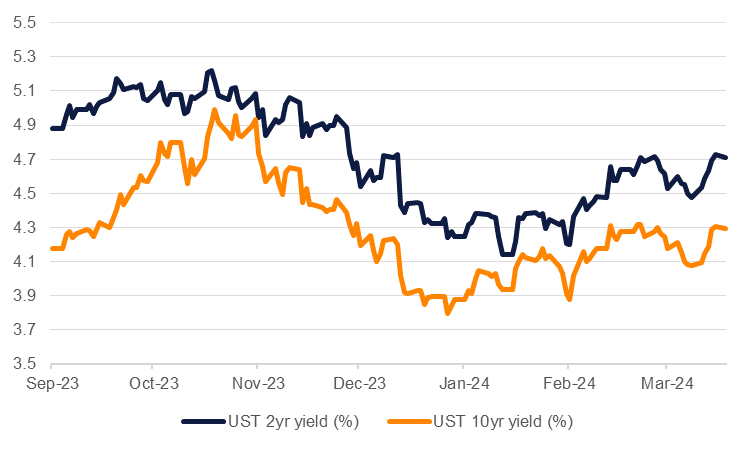

Given the bias of the Fed to seemingly err on the side of being “higher for longer” there is a risk that the dots plot could be revised to show 50bps worth of cuts in total for the Fed Funds rate in 2024. Anticipation of that risk seems to have been behind the upswing in US Treasury yields since the start of the year: yields on the 2yr UST have risen by 46bps since the end of December to 4.71% while the 10yr yield has jumped by about 42bps to about 4.30% in the same period with a more than 20bps hike in yields for both securities in the last week alone.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

There is also likely to be focus on when the Fed will signal whether its balance sheet runoff can slow and ultimately come to an end. In the minutes of the January 2024 FOMC “survey respondents expected a slowing of the pace” by July and that the size of the remaining balance sheet was “slightly higher” than had been estimated in December 2023. At the December press conference after the FOMC, Chair Powell said the Fed would continue to reduce its holdings until “reserve balances had reached a level somewhat above that consistent with ample reserves” but that the Fed didn’t judge that it was yet at those levels.

Edward Bell

Edward Bell