Recent Search

Popular Searches

Although the 10-year US Treasury yield has fallen back below 3.0% this week, it is still close to its highest level since 2012 and more than double of where it was two years ago. On several other occasions in recent years, the yield had climbed to around 3.0% only to fall back again. However, this time around we think the yields may stay at these elevated levels for few months to come, for several reasons as discussed below.

The annual US budget deficit is likely to exceed $1 trillion by fiscal 2020, from about $666 billion in 2017 as revenue gets reduced due to the recent tax overhaul and expenditure gets increased to fund the proposed infrastructure spending. In order to fund budget deficits, the US Government debt sales are set to swell.

The US Treasury had earlier released data showing it would need to borrow $955 billion in 2018, and more than $1 trillion in the two subsequent years. Those sums are considerably higher than last year's $516 billion in new debt issued.

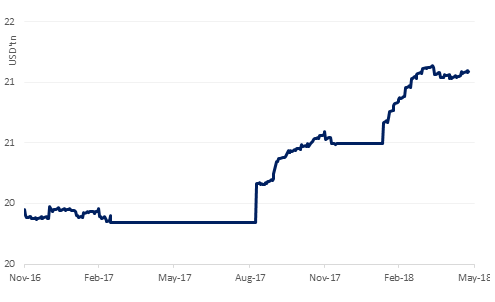

In contrast, the demand for treasuries is unlikely to keep pace with the supply and in-fact may drop from the current level.