Recent Search

Popular Searches

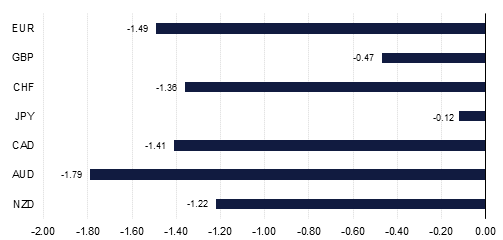

A strengthening US economy combined with the prospect of extended easy money in the Eurozone saw the EURUSD lose significant ground falling 0.5% on Friday and 1.5% since the start of the week. The USD benefited from stronger than expected Q3 GDP growth of 3.0% along with developing optimism about corporate tax cuts, and the possibility of hawkish Professor John Taylor being appointed as Fed Chair in the coming week. The EUR meanwhile struggled under the twin burdens of deteriorating political events in Spain and from the ECB’s announcement that it would extend its bond buying scheme until September 2018 at least, and probably beyond.

In the coming week the focus will be on the Fed, but even if Taylor is not nominated to take over from Janet Yellen the dollar is unlikely to react too adversely. An interest rate rise in December now looks relatively assured, and the markets may even start to wonder why the Fed will wait and not tighten policy again this week. But more importantly markets may also begin to believe the Fed dots for 2018 which imply that it will raise interest rates a further three times. Currently the markets are only pricing in the one further interest rate hike next year, but there is little reason to believe that any of the three main candidates for Fed Chair will deviate from the Fed’s current working assumptions, at least not dovishly.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

US data in the coming week may to some extent get overshadowed by the Fed announcement but it should also provide evidence that Q4 is beginning as equally strongly as Q3 ended. ISM activity readings are expected to remain close to historic highs recorded last month and the employment report is expected to show payrolls bounce back strongly after the hurricane impacted weakness seen in September, with 310k of new jobs anticipated. All of this should help to keep the dollar’s tone firm and not only against the Euro.

However, the single currency can still be expected to bear the brunt of this strength given the complicated political picture in Spain’s Catalonia and the uncertainty about what will happen next. After Catalonia’s parliament declared independence last Friday, Madrid has moved quickly to assert administrative control over the rebellious region.

The likely objective will be to hold new regional elections in the coming months but keeping the situation calm will not be easy especially if arrests follow which seems likely. The relevance for the broader EU is contained in the warning from the EU Commission President Jean-Claude Juncker who said that the EU ‘has no room for further fractures’. With the Greek crisis still fresh in people’s minds the EU cannot afford another existential crisis that threatens the integrity of the bloc, especially with populist anti-EU parties gaining ground across a number of EU member countries.

The EUR also remains heavy following the ECB’s announcement last week about extending QE well into next year. Although the quantum of asset purchases was halved to EUR30bn per month, an absolute end date was avoided with Draghi suggesting that they will not abruptly stop QE in September 2018. Considering this interest rate rises will probably also not be considered until 2019 at the earliest. The preliminary estimate for Q3 Eurozone growth will be released on Tuesday with the possibility that this will fall back to 0.5% q/q from 0.7% in Q2, which may also not help sentiment around the single currency, particularly in light of stronger than expected GDP readings elsewhere. The next target for EURUSD would appear to be 1.15, which in some ways might only be a stepping stone before the 200-day moving average comes into focus, currently standing at 1.1245.

An example of stronger than expected GDP is in the UK where preliminary Q3 GDP expanded 0.4% q/q, up from Q2’s 0.3% q/q and compared to a forecast of 0.3% q/q, but with annual growth unchanged from Q2 at 1.5% y/y. The service sector grew by 0.4% q/q, while manufacturing rose by 1.0% and the construction sector contracted for a second consecutive quarter. As well as being cheered by this performance the Bank of England , which meets this week, will also be reassured by the more upbeat global outlook, such that it should feel able to raise interest rates by 0.25%, for the first hike in a decade. However, Bank officials will likely strike a relatively cautious tone about 2018 and emphasize that any further moves will be gradual. This should prevent the pound from rallying too strongly on the decision and we would not even be surprised if it fell back to test its key support around 1.30 in the short term.

Gradualism was also in evidence in Canada last week, where after surprising with a rate hike in September the Bank of Canada left policy on hold and struck a cautious tone about tightening prospects going forward. When asked about the likelihood of another rate hike BOC Governor Poloz said ‘there are a lot of things that have to come together before we feel confident that we're all the way there.’ The data calendar in Canada in the coming week is a relatively busy one with August GDP, September trade and October jobs all due out. The BOC’s caution, however, suggests that it will take a lot to alter its gradualist course, a message that is likely to be repeated by the Governor when he speaks again before parliament. With January now becoming the next favorite month for another rate move, there is scope for USDCAD to continue to rise as the markets increasingly discount the Fed moving beforehand.

As for Australia the RBA is also playing things safe against a backdrop of unspectacular inflation, which dipped to 1.8% y/y in Q3 helping to dissuade markets about any urgency the RBA might have to make a policy adjustment. This is also likely to keep AUD sentiment heavy with the break of the 200-day moving average last week keeping the risks pointed towards the mid-0.75s, and 0.74 thereafter.

Finally following the landslide election in Japan last week the Bank of Japan meets in the coming one and is likely to recommit to ultra-accommodative policy settings, especially as CPI remains far below its 2.0% target and will likely remain so through next year. Headline and core CPI inflation remained at 0.7% in September, while excluding fresh food and energy it stands at just 0.2%, and the BOJ is likely to revise down its inflation forecast for the year underlining the monetary policy challenges that lie ahead. The JPY should remain pressured as a result, and as we pointed out recently it has a long standing track record of softening in the fourth quarters of years. Continuity in Asia was also reinforced by President Xi’s consolidation of power in China, but the data flow should be muted in the coming week with only PMI data for October on the calendar.

Click here to Download Full article