Recent Search

Popular Searches

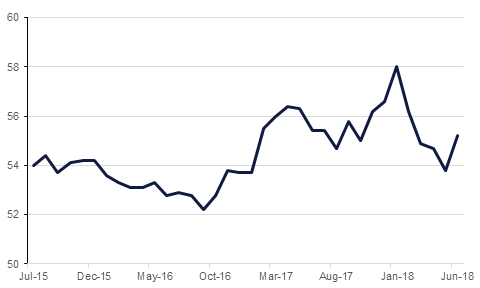

Eurozone services PMI exceeded expectations in June, coming in at 55.2, up from 55.0 the previous month. This is more positive data for the Eurozone, following some disappointing results in manufacturing PMI and retail sales earlier in the week. UK services PMI also beat expectations, at 55.1 compared to 54.0. This is positive news for Prime Minister Theresa May as she convenes her cabinet for a Brexit summit on Friday, with the aim of submitting a white paper next week. The PM’s new Brexit plan is reportedly an amalgamation of the two customs options that were under examination by her cabinet working groups - namely maximum facilitation and the customs partnership. Labelled the facilitated customs agreement, it will collect tariffs for the EU on its border, but the use of technology will minimise bureaucracy. It is worth noting that the EU previously considered both of these options unworkable, and Brexit secretary David Davis has reportedly told May that the new option is also unviable.

US non-farm payroll numbers for June are due on Friday. Consensus expectations are for a boost of 195,000 jobs, compared to the 223,000 added to the payroll in May. Unemployment is anticipated to stay at the 3.8% recorded last month, which was the second-lowest level since 1969. While data from the US so far this week has been strong, anecdotally, firms are anxious about the effect of tariffs on their businesses, and core capital investment has expanded at a slower pace. With USD 34bn of tariffs on China set to be introduced tomorrow – and China has promised to retaliate – the rising tensions could soon come to impact the jobs numbers.

Morocco has put a cap on fuel prices, as their contribution to rapidly rising inflation has prompted protests. While inflation, at 2.6% y/y in May, is comparatively low in the region, it is at its highest rate in five years. Many MENA oil importers have seen protests over the rising cost of living in recent months, as government efforts to curb subsidies have coincided with the recent climb in global oil prices, squeezing households’ spending power.

Regional bonds closed largely unchanged with the YTW on the Bloomberg Barclays GCC Credit and High Yield index remaining at 4.59% and credit spreads flat at 192 bps.

There is renewed pressure on Bahrain bonds with 5 year CDS jumping 13 bps to 442 bps. It has gained +10.0% over the last five days despite assurance of support from Saudi Arabia, Kuwait and the UAE. Bahrain 21s dropped 1 point to USD 98.0 while Bahrain 28s fell 1.5 points to USD 88.0.

The board of Union Properties has approved an AED 500mn sukuk issuance.

The USD index is a touch weaker going into a big weekend. The US is set to impose trade tariffs on China tomorrow, and the market also awaits the June payrolls data. There was little movement in G7 currencies overnight with the US markets closed since Wednesday afternoon.

The Chinese renminbi continues to be supported by PBOC, which strengthened the reference rate for the yuan by 0.62% to 6.6180/USD and also drained liquidity through open-market-operations today.

It was a subdued day of trading for developed market equities as US markets were closed. The Euro Stoxx 600 index added +0.1%.

Regional equities closed higher with the DFM index adding +0.8% and Kuwait Premier Market gaining +2.6%. The rally in Kuwait was led by market heavyweights with National Bank of Kuwait and Zain adding +2.0% and +4.5% respectively. Elsewhere, Drake& Scull broke out of the cycle of closing limit down with gains of +3.3%.

US President Trump tweeted about oil prices again last night, calling on OPEC members to ‘REDUCE PRICING NOW.’ Brent futures fell 0.7% to USD 77.66/b, while WTI fell 0.4% to USD 73.82/b. The weekly EIA report will be published later today rather than on its customary Wednesday, owing to the July 4 holiday yesterday.

Click here to Download Full article

Daniel Richards

Daniel Richards