Recent Search

Popular Searches

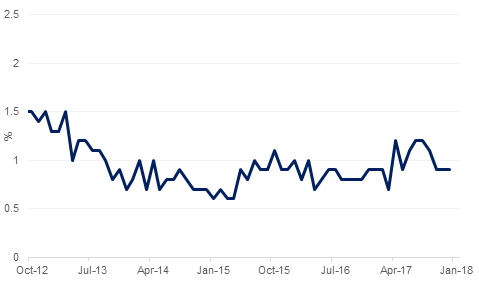

The core measure of underlying inflation in the Eurozone was unchanged in December from the previous month’s reading of 0.9% y/y. This is the third consecutive month at that rate and is unlikely to prevent the European Central Bank from abandoning its commitment to keep expanding asset purchases until prices start rising faster. The headline CPI at 1.4% reflected slight deceleration from the 1.5% reported for November. On a countrywise basis, YoY headline inflation was 1.5% in Germany, 1.2% in France but only 0.5% in Greece.

Unemployment rate in December in Australia increased to 5.5% from 5.4% in November even though total number of jobs added were higher than expectation. The increase in unemployment rate is largelly due to increased participation rate from 65.5% to 65.7%. Australia's strong hiring momentum, if sustained into 2018, should start to lift wage growth and fuel expectations of tightening by the central bank. Currently RBA is expected to leave its cash rate target unchanged at 1.5% over the next few quarters.

Bank of Canada raised rates by 25bps, taking the policy rates to 1.25% but indicated that it’s in no rush to pursue aggressive interest rate hikes due to “important unknowns” such as the future of Nafta. This was the third rate hike in Canada since July last year as the country’s solid economic growth fuels surge in employment.

In the US, Government funding runs out on Friday and the House and Senate are heading towards a temporary extension to February 16. Democrats are demanding that spending legislation include a provision permanently shielding about 690,000 undocumented immigrants brought to the U.S. as children from deportation. However market expectation is that Democrats will not stop the extension from happening because of this demand. By mid February, Congress is expected to come up with a broader budget agreement for the rest of the fiscal year.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

UST yield curve recorded bear steepening yesterday with yields on 2yr treasuries rising three bps to 2.05% and that on 10yr rising five bps to 2.59% as corporate result announcements indicated several companies intending to bring money back home and increase jobs in the country. Across the pond, increase in government bond yields were more subdued with 10yr Gilts and Bunds closing at 1.31% (+0.5bp) and 0.56% (unchanged). Credit spreads were largely unchanged with CDS level on US IG and Euro Main finishing the day close to thier opening levels at 48bps and 44bps respectively.

Regionally GCC bonds moved in sync with benchmark yield widening. Average yield on Barclays GCC index increased a bp to 3.70% though credit spreads tightened a bp to 127bps.

Earning announcements remained uneventful. Activity in the primary market has been low this week, however, looking ahead, Emirates NBD has mandated banks for a Formosa bond and Egypt Sovereign is planning a Eurobond in early February.

AUD has fallen from an almost four month high in the aftermath of employment data which showed the first increase in unemployment since June 2017 (see macro). As we go to print, AUDUSD trades 0.14% lower at 0.79601, reversing yesterday’s gains. We see further declines in the short term with initial support coming in at 0.7937, the 76.4% one year Fibonacci retracement. A break of this level is likely to result in a retest of levels below 0.79.

Elsewhere, USD continues to trade firmer against JPY amid speculation that the US may be able to avoid a government shutdown. Since yesterday USDJPY has gained 0.88% to climb to 111.42, taking the cross back above the 38.2% one year Fibonacci retracement (110.49), following an unstained break of this level on Tuesday. We expect further gains to lie ahead with the first level of resistance coming near the 200 day moving average of 111.74.

Global equities were mixed with all indices in US closing higher though Europe failed to follow suit. Strong earning announcement pushed Dow Jones up by 1.25% and S&P 500 by 0.94%. In contrast European bourses generally gave up their previous days gains without any material trigger. FTSE 100 closed down by -0.39% and Dax by -0.47%.

In line with strong session in the US, Asia has opened in the green this morning. Hang Seng is up 0.56% at the time of writing.

Regional equities were mixed. DFM and Abu Dhabi exchanges were each up by over 0.4% followed by Tadawul at +0.17%. However Qatar and Kuwait indices were marginally in the red.

Oil prices eased overnight with benchmark Brent futures declining 1.6% to move back below USD 70/b while WTI closed at USD 63.73/b, down 0.9%. There have been few fundamentals to push the market around this week and weekly data from the EIA will be delayed owing to a public holiday in the US at the start of the week. The EIA did publish their drilling productivity report overnight and expect oil production from shale assets to reach 6.55m b/d in February, up more than 110k b/d month on month.