Recent Search

Popular Searches

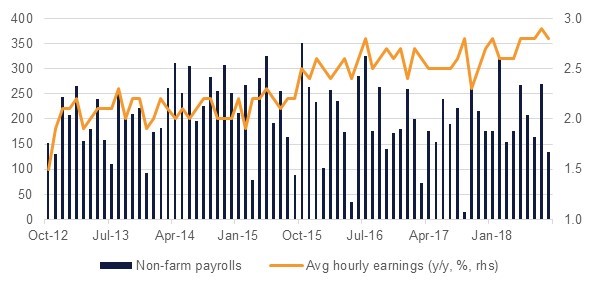

Inflation in the Eurozone picked up to 2% in June while core inflation slipped to 1.2% from 1.3% a month earlier. The general trend up in inflation will reassure the ECB that it can carry on with winding down bond purchases and keep a message that policy normalization will begin at some point in mi- 2019. In the UK inflation data held steady at 2.4% in June even as fuel prices rose to their highest level since September 2014. The standstill on inflation will raise doubts about whether the BoE will raise rates as expected at its upcoming meeting in August. Producer price inflation, however, accelerated and rose by 3.2% y/y in June compared with 2.9% a month earlier. The pick-up in PPI will likely feed into higher prices going forward and put the BoE back on a rate rising path.

Japan’s exports dipped in June to growth of 6.7% compared with more than 8% growth previously. Overall export growth is running slower in 2018 than at the same time last year as trade concerns are weighing on export demand. Car exports fell 12% y/y including sales to the US. A survey of business sentiment, the Reuters Tankan index, fell in its latest reading as firms became concerned about the impact of a trade war on their business.

The US is now producing 11m b/d of crude oil for the first time ever, taking it well above Saudi Arabia and putting it on pace with Russia as the world’s largest producer. Production growth remains at an elevated pace, up 1.5m b/d or 16% on the same time last year. Output continues to push past government projections for growth and continued, albeit slower growth, is expected in 2019. However, physical pricing in the key growth region—the Permian basin in Texas—still remains weak at just USD 55.78/b this week, USD 13/b below WTI benchmark prices. This level leaves very little headroom for the development of new wells in the region and could temper production growth rates more than currently projected.

Source: EIKON, EIA, Emirates NBD Research

Source: EIKON, EIA, Emirates NBD Research

Treasuries remained slightly lower but in a departure from the recent trend, the front end outperformed the long end of the curve. Yields on the 2y UST, 5y UST and 10y UST closed at 2.61% (flat), 2.77% (+1 bp) and 2.87% (+1 bp) respectively.

Regional bonds continued to trade in a tight range. The YTW on the Bloomberg Barclays GCC Credit and High Yield index closed at 4.47% (+1 bp) and credit spreads remained flat at 175 bps.

In terms of rating action, Fitch affirmed Mubadala Development and IPIC’s ratings at AA with stable outlook. Moody’s affirmed the rating of Dolphin Energy at A2 and changed the outlook to stable from negative.

Elsewhere, Saudi Electricity is said to be in talks for a USD-denominated bond sale as the company looks to refinance a USD 2.6bn bridge syndicated loan raised in January.

It was largely a day of USD strength as markets reacted to Fed Chair Jerome Powell’s comments on the US economy. Powell said he expects the economy to remain on course for steady growth, largely in line with market views that more interest rates are expected this year. Softer than expected inflation in the UK cast doubt on the Bank of England’s decision at its next MPC meeting and helped push GBP to a new low for the year. Sterling is holding levels close to 1.30 and will remain highly sensitive to political headlines.

In the Antipodes, AUD is up strongly this morning after a strong jobs report. More than 50k new jobs were added in June compared with market expectations of 17k and has helped push AUD up to 0.7425.

Developed market equities closed higher as the start of the earnings season continue to remain strong. The S&P 500 index and the Euro Stoxx 50 index added +0.2% and +0.8% respectively.

Regional equities closed mixed with the DFM index adding +0.6% and the Tadawul losing -0.1%. The DFM index was buoyed by strong earnings from Emirates NBD (+2.0%). Dubai Islamic Bank dropped -0.4% even as the bank reported +14.6% y/y increase in net profit in Q2 2018. Elsewhere, Jabal Omar and Tasnee lost -3.0% each.

Oil prices gained around 1% across both contracts last night thanks to drop in gasoline inventories in the US. Oil production in the US has now hit 11m b/d for the first time ever while inventories increased upward despite ongoing disruptions to imports from Canada.

Brent markets continue to remain in contango for the first two months of the forward curve while the backwardation in WTI held at around USD 1/b.

Click here to Download Full article