Recent Search

Popular Searches

Eurozone’s final CPI in June reflected that inflation decelerated further in the region, down to 1.3% y/y compared with 1.4% in May and 2.0% recorded in February this year. However core CPI – excluding energy, food, alcohol and tobacco strengthened to 1.1% y/y compared with 0.9% in May. Of further comfort to the central banker would be the core inflation excluding energy & processed food but including tobacco & alcohol (ECB’s preferred measure of core inflation) came in 1.2% y/y – highest in over two and half years. No material change in policy is expected to be announced at the ECB meeting this Thursday.

July Empire Manufacturing Index in the US fell 10 points in July to 9.8 though not too far from the 1H average of 11.5. The number suggest a continued expansion on the factory floor, which will contribute favorably to aggregate demand in the second half, however the pace has reduced somewhat as manufacturers are coming to accept that the Trump administration may not adopt any of the anticipated stimulus measures it initially planned.

In Australia, June meeting minutes reflect that RBA sees neutral policy rate to be lower at 3.5% vs the previous estimate of 5%. Though the current rate of 1.5% appears still very accommodative, RBA is likely to stay put in the short term in view of the current currency strength and uncertainty about how the global events will impact Australian economy going forward.

Later today we expect UK CPI data to show that inflation held steady in June and continues to exceed BoE’s target as a result of weak currency even though recent decline in oil prices would see headline CPI remaining below 3%. Headline number is expected to be around 2.8% and core CPI at around 2.6%. Despite the Brexit risk, inflation in the UK is amongst the highest in the developed world which may force BoE to move on rates faster than the current expectations.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

|

| Time | Cons |

| Time | Cons |

| UK CPI y/y | 12:30 | 2.6% | US Housing market index | 18:00 | 67 |

| EC Zew Survey Expectations | 13:00 | NA | GE Zew Expectations | 13:00 | 88 |

Source: Bloomberg.

Stagnation of policy measures in the US and decelerating headline inflation lead to further flattening of the UST curve with yields on 2yr, 5yr, 10yr and 30yr treasuries closing at 1.36% (unchanged) , 1.86% (-1bp), 2.32% (-1bp) and 2.90% (-2bps) respectively. With limited risk of faster rate hikes, credit risk was well bid. CDS levels on US IG and Euro Main closed tighter by a bp each at 58bps and 54bps respectively.

Locally GCC bonds were flat yesterday with average yield on Bloomberg Barclays GCC index closing unchanged at 3.46% and credit spread at 148bps.

In corporate news, Emirates Airlines signed partnership agreement with Fly Dubai. Partnership goes beyond code-sharing and includes integrated network collaboration with coordinated scheduling. The combined network of the two sister airlines is expected to reach 240 destinations by 2022.

Fitch downgraded Kuwait Energy from B- to CCC, citing deteriorating financial profiler due to market conditions not allowing completion of the IPO in 1H2017. KUWAIE 19s closed unchanged at YTM of 12.7%. In another news, S&P has assigned BB rating to Dubai Aerospace with positive outlook.

The dollar has continued to build on 2017’s declines, with the Dollar Index reaching a new YTD low of 94.71. The dollar wiped out yesterday’s gains and was sold off following a Health-care Bill setback after an additional two Republican senators voiced opposition to the proposed overhaul. The biggest declines were against the AUD which found support following the release of the RBA minutes which were mildly positive as, despite lowering the neutral interest rate to 3.5%, the central bank cited that downside risks are receding to some extent.

As we go to print, AUDUSD trades 1.09% higher at 0.78848, off earlier highs of 0.7904, levels last seen in December 2014 and has effectively broken out upwards from its former daily uptrend channel. While the pair continues to trade above 0.7723, the five year 23.6% Fibonacci retracement, the risk of a rise towards 0.8278 remains substantial. In addition, the 50 day moving average (MA) has completed a golden cut on the 200 day MA and is in the process of crossing the 100 day MA in the same way, indicating that further upside can be expected. One initial limitation is that that the 14 day Relative Strength Index (RSI) of 75.61 indicated that the pair is overbought and that some profit taking may provide an initial hurdle to further gains.

Global equities had soft start to the week yesterday with S&P 500 falling 0.04% mainly as a result of weakness in healthcare stocks in response to further delay in healthcare reforms in the US. Though Euro Stoxx 50 had little to hinge on to falling by 0.27%, FTSE 100 was up 0.35% with economy doing better than expected. Across in Asia, Topix and Hang Seng both slid 0.9% and 0.2% respectively.

Regionally, Dubai index was buoyed by purchases in the real estate and banking shares ahead of expected good results from these sectors. Abu Dhabi index also closed up by 1.14% lead by bank and energy sectors. In contrast, Tadawul reversed some of its previous gain, closing down by 0.61% as oil prices softened overnight.

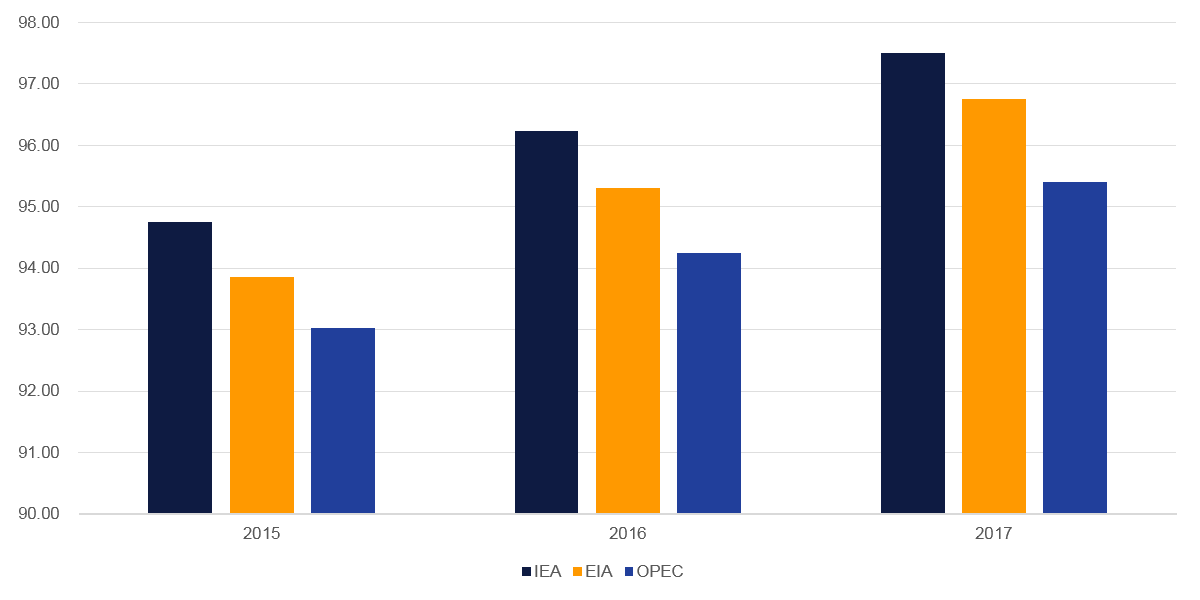

Oil futures were little changed, trading at near $46 a barrel even though output from major U.S. shale plays is expected to reach 5.58 million barrels a day in August, an all-time high. Libya has also increased production to 1.1 million barrels a day.

Gold climbed 0.3 percent to $1,237.60 an ounce.

Click here to download full article