Recent Search

Popular Searches

Mixed industry data out of the US combined with some dovish commentary from Fed officials will give the market pause as it assesses the trajectory for rates going forward. Factory orders in July dropped 3.3%, their largest decline since August 2014. However, capital goods demand improved in July and if volatile aircraft purchases are stripped out, demand rose 1% m/m. The data clouds the picture somewhat over how much of a contribution investment will contribute to GDP growth in Q3 in the US. However, industry output will likely pick up in the final quarter of the year as cars, houses and infrastructure damaged by Hurricane Harvey will need to be replaced, providing some support for manufacturing.

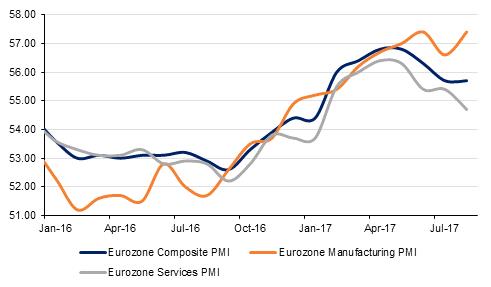

Official estimates for Eurozone business activity in August showed a strong performance as the improvement in the regional economy continues. The composite PMI level for August hit 55.7, only slightly lower than the initial flash estimate, and forward looking components of the PMI indicate that Q3 will end with some vigour. Among the core economies of Germany, Italy and France, all showed solid growth in August with levels comfortably in expansion territory. The August figures will likely be taken as encouragement by the ECB, which meets on Thursday, to provide more details about how and when it will begin to drawdown on stimulus measures. In the UK, however, PMI figures are pointing to further slowing in the economy. The August services PMI fell to 53.2 from 53.8 a month earlier contrasting with positive figures that had come out of the smaller manufacturing sector earlier.

The Reserve Bank of Australia kept rates unchanged at 1.5% yesterday in line with market expectations. The RBA governor gave a positive assessment that economic growth was accelerating and would hit 3% in coming quarters. Government spending has helped support growth in the near term while commodity prices have improved in Q3, helping to support a positive outlook for exports. The Australian economy expanded 0.8% q/q in Q2 thanks to government and consumer spending. Improving metals will help to provide some support for the current quarter.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

|

| Time | Cons |

| Time | Cons |

| UAE Emirates NBD PMI | 8:15 | n/a | US Composite PMI | 17:45 | n/a |

| CA Rate decision | 18:00 | 0.75% | US ISM non-manf comp | 18:00 | 55.5 |

Source: Bloomberg

Three Fed officials dampened prospects for another rate hike this year, questioning the need for higher rates while inflation is actually slowing according to the Fed’s preferred price gauge. Governor Lael Brainard said the Fed should see prices pushing above its target of 2% before moving rates, echoing comments from Dallas Fed president Robert Kaplan who said the Fed can “afford to be patient.” Even more dovish commentary came from the Minneapolis Fed president, Neel Kashkhari who suggested that rate hikes have been damaging the economy over the last 18 months, contributing to lower wage growth.

In response to the Fed commentary yields dropped steadily from the middle of the curve onward. Yields on 10yr USTs fell 9bps, contributing to a flattening of the 2-10 spread to 78bps, its lowest level in nearly a year. The decline in benchmark yields also accelerated on the back of risk-off moves as geopolitical tensions have risen further following threats from North Korea after its latest nuclear test. Gilt and bund yields dipped in line with USTs.

Regional markets were quiet with no new primary issuances or rating actions though Doha bank is believed to be seeking external debt.

USD has come under pressure in the aftermath of Federal Reserve officials urging caution on the pace of further normalization of monetary policy. Minneapolis Fed President Neel Kashkari highlighted the risks of further tightening while Fed Governor Lael Brainard urged patience on the timing for a further rate hike.

As we go to print, the Dollar Index currently trades at 92.32, a 0.61% decline so far this week and reinforcing the daily downtrend that has been in effect since 3 January 2017. At these levels, the index looks technically vulnerable and a retest of the one year lows of 91.62 remains a possibility in the near term. A break and daily close below this level would expose the index to further downside, with declines towards the 38.2% five year Fibonacci retracement of 88.24 becoming a possible scenario.

Markets swung sharply to risk-off trades yesterday as the impact of North Korea’s latest nuclear test and the country issued further threats to the US. The S&P 500 closed nearly 0.8% lower while the FTSE lost 0.5% and the Nikkei closed 0.6% down. Regional markets were largely unchanged: the DFM fell 0.3% and the ADX close 0.1% lower.

Oil markets recovered strongly yesterday on expectation that US refinery demand would begin to normalize quickly. Brent prices closed nearly 2% higher and are back to holding a USD 53/b handle. Oil prices may receive another boost near term if Hurricane Irma, currently in the Atlantic crosses into the Gulf of Mexico where it is more likely to damage oil producing regions than Harvey, which hit refineries more severely.

Industrial metals cooled somewhat yesterday as nearly all prices remain strongly in over-bought territory. Copper prices are likely to be carried to US 7,000/tonne on the momentum currently in the market, setting up for a more precipitous fall if they indeed push much higher.