Recent Search

Popular Searches

President Trump threatened tariffs on more Chinese imports, ordering officials to identify $200 billion of goods for additional levies of 10%. On the other side, the Ministry of Commerce in Beijing said it would retaliate with "strong" counter measures. The developments suggest a deepening trade dispute that the International Monetary Fund has described as one of the biggest risks to global growth. While the hit to growth around the world has so far been limited, the danger is that confidence and sentiment will soon start to sour and limit corporate expansion and investment plans. The U.S. imported $505 billion of goods from China last year and exported about $154 billion. The fact that America imports more from China will make it harder for Beijing to match President Trump’s attacks, however, China could look at its investment in US treasuries and other FDI made into the country as other negotiating tools.

The NAHB Housing Market Index in the US fell to 68 from 70 in the previous month, reflecting weakening of sentiment on the back of rising input costs, partly as a result of new tariffs. Staying on the housing front, asking house prices in the UK in June rose 0.4% m/m taking the y/y growth to 1.7%. However, house prices in London remained under pressure falling –0.9% m/m, -1% y/y as Brexit fears continued to dampen demand. In Australia, residential property prices fell 0.7% q/q in the first quarter of this year, although still 2% above the previous years level.

OPEC members are reportedly considering raising output between 300k b/d – 600k b/d in order to offset the decline in production from Venezuela. Only a few countries within OPEC are able to raise production easily and among the GCC producers, such an increase would take them to roughly 100% compliance with the OPEC+ production cut deal. Our expectation for Friday’s meeting is that hitting full compliance will be the ceiling for any production increase as it allows for the existing deal to remain in place and increase in output by some members.

According to the data from TurkStat, Turkey’s unemployment rate fell to 10.1% in March, from 10.6% the previous month and compared to 11.7% a year earlier. This marked the lowest level since May 2016, and follows data released last week showing that GDP saw real growth of 7.4% in the first quarter. However, survey results from Turkey’s purchasing managers’ index showed signs of firms job shedding in May, suggesting that the unemployment rate may have bottomed out.

Treasuries traded in a tight range as the recent trend of the long end of the curve outperforming front end continued. Yields on the 2y UST, 5y UST and 10y UST closed at 2.54% (flat), 2.79% (flat) and 2.91% (-1 bp) respectively.

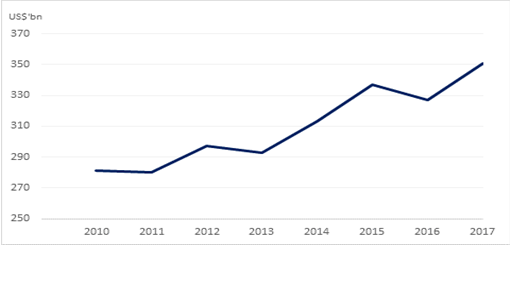

Regional bonds continued to drift lower. The YTW on the Bloomberg Barclays GCC Credit and High Yield index jumped +3 bps to 4.66% and credit spread widened 2 bps to 1.91%.

Fitch said that Abu Dhabi’s new economic stimulus of AED 50bn will have limited sovereign credit impact given its strong balance sheet and low fiscal break-even oil price. The rating agency expects budget surpluses of 3.2% of GDP in 2018 and 0.9% in 2019 for Abu Dhabi.

JPY has rallied this morning, gaining on all the other major currencies after China reacted to a fresh set threats from U.S. President Trump to impose more tariffs on goods has escalated trade tensions between the two countries. As we go to print, USDJPY 0.63% lower at 109.86 in a move that has taken the price back below the 200 day moving average (110.25) for the first time in five days. We anticipate support beginning to exert itself at the 50 day moving average of 109.34. A weekly close below this level will increase the risk for additional declines towards 108.44. On the other hand, a daily close above the 50% one year Fibonacci retracement (109.65) may result in a reattempt at the 200 day moving average, followed by a retest of the resistive 110.85 level, which sits at the 61.8% one year Fibonacci retracement.

As a consequence of investor concern over trade escalations, AUDUSD is trading lower, AUDUSD losing 0.14% during the Asia session to reach 0.74128 and on target to fall for a fourth potential day. Of note is that the price reached a new 2018 low (0.7394) earlier in the session. While the daily closes remain below 0.7519 (the 23.6% five year Fibonacci retracement), the chances of further declines towards 0.72 cannot be ruled out.

Developed market equities closed lower as political tensions in Europe and trade tensions between the US and China weighed on investor sentiment. The S&P 500 index and the Euro Stoxx 600 index dropped -0.2% and -0.8% respectively.

Most regional equities were closed. The DFM index and the ADX index dropped -1.8% and -2.7% respectively. Air Arabia dropped -7.1% following reports that the airline has exposure to Abraaj. The company said in a statement that it has appointed a team of experts to protect its investment in Abraaj funds. The company did not specify the size of investment.

Oil halted previous day’s losses, as OPEC members are considering raising output by a more modest amount than previously discussed. Brent closed up at $74.86 pb.

Precious metals gained amid renewed concerns over trade protectionism after President Trump threatened to impose more tariffs on Chinese goods. Gold was up 0.2% to $1281.29/oz and silver closed up by 0.4% to $16.54/oz. In contrast, China's raw materials futures -- iron ore, copper, zinc and aluminium -- are all trading lower today.

Click here to Download Full article