Recent Search

Popular Searches

Global equities had their best week of 2024 as economic data showed that the US economy continues to remain resilient amid easing inflationary pressure as indicated in the latest CPI reading. Overall, the MSCI World index added +4.0% 5d on the back of strength across all markets but particularly in developed markets. The MSCI G7 index added +4.1% 5d.

The focus of investors this week will be on Federal Reserve Chairman Jerome Powell’s speech at the annual Jackson Hole symposium. Given that financial markets have calmed down, it is widely expected that he will reiterate the message of being data dependent ahead of the September Fed meeting where the central bank is now widely expected to cut interest rate by 25 bps. Beyond that, investors will continue to keep an eye on geopolitical developments and minutes from the last Federal Reserve and European Central Bank meetings.

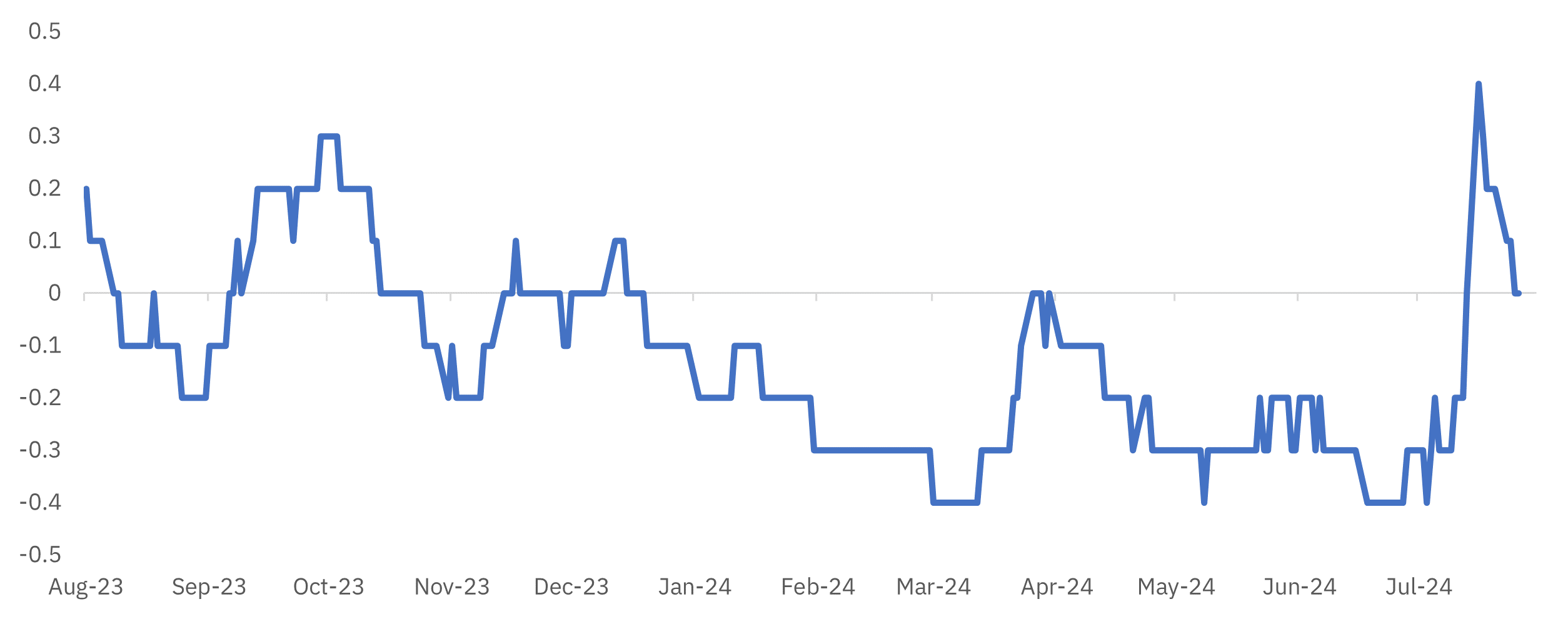

The cross-asset volatility as measured by the BofA Securities GSFI Market Risk index reverted to mean at the end of last week after jumping to a 1-year high at the start of the previous week. It must be noted that levels less than 0 indicate less stress than normal.

The same is also corroborated by sharp declines in the VIX index (-27.3% 5d), the V2X index (-29.2% 5d), and the CBOE Emerging Market ETF Volatility index (-27.3% 5d).

Source: Bloomberg

Source: BloombergRegional equities followed the global trend and closed higher. The S&P Pan Arab Composite index added +1.5% 5d. The ADX index was a notable exception with a drop of -0.2% 5d.

As we come to the end of the Q2 2024 earnings season in the UAE, it is worth noting that du (+8.6% 1m) along with financial sector stocks (+6.7% 1m) have been best performers on the DFM over the reporting period. Utility sector stocks also recouped some of their year-to-date losses with gains of +4.1% 1m.

Elsewhere on the Tadawul, only utilities and real estate sector stocks gave positive returns over the reporting period with gains of +2.7% 1m and +2.5% 1m respectively.

Aditya Pugalia

Aditya Pugalia