Recent Search

Popular Searches

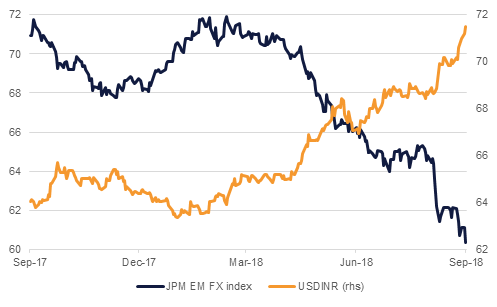

Markets are struggling to avert their gaze from trade war and emerging market related issues that are hurting sentiment and raising questions about whether the Fed will continue to tighten monetary policy. President Trump is apparently struggling to face down Canada in trade negotiations, while at the same time EM currencies are continuing to feel the heat. In particular EM currencies that are under most pressure are those with high current account deficits and with large foreign currency borrowings, built up during the last decade of low rates but which are now showing signs of stress amid the Fed's tightening cycle.

The Indian rupee has hit a new record low, while the Indonesia's rupiah hit a new 20-year low near to the 15,000 levels last seen during Asian crisis of 1997-98. South Africa's rand lost another 2% falling to a three-week low as data showed the economy contracted by 0.7% q/q putting it in a recession, while the Turkish lira, Russian rouble and Mexican peso all posted more losses yesterday. The Argentinian peso fell a further 3% with the government in talks with the IMF and despite it announcing "emergency" austerity measures.

The monthly flow of activity data were the other main developments yesterday, which in the US cases only adds to the likelihood of the Fed tightening monetary policy at its next meeting on the 26th September, potentially making life harder for EM. The ISM manufacturing index rose to 61.4 from 58.1 in July, to reach a 14-year high. The rise was driven by a surge in the new orders index to 65.1, from 60.2, while the employment index rose to 58.5 from 56.5 last month, and the production component rose to 63.3 from 58.5.

Regional PMIs were broadly steady in August, easing a little in the UAE, edging up in KSA and improving in Egypt. The main takeout from a UAE perspective was that the drag on the overall headline index (to 55.0 from 55.8) was largely due to a decline in average employment – the first time this has been recorded since the survey began in August 2009. While this may seem surprising in the context of what appears to be steady output, the greater surprise is perhaps that output is holding up as well as it is.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Treasuries closed lower with the curve bear steepening following better than expected economic data. Yields on the 2y UST, 5y UST and 10y UST closed at 2.65% (+3 bps), 2.77% (+3 bps) and 2.89% (+4 bps) respectively.

Regional bonds drifted lower following broad trend in USTs. The YTW on the Bloomberg Barclays GCC Credit and High Yield index jumped +4 bps to 4.48% and credit spreads remained flat at 174 bps.

S&P lowered its credit rating on DEWA to BBB from BBB+ and on DIFC to BBB- from BBB. The outlook on DEWA rating is negative and stable on DIFC rating.

EM FX continued as the main mover yesterday, with the JPMorgan EMFX index hitting historic lows (see front page). This helped to keep the USD supported against developed currencies as well, although these movements were less pronounced, with the EUR broadly steady and with GBP being the main major currency at risk in view of recent uncertainty about Brexit and in the wake of poor UK economic data.

Yesterday saw the UK August construction PMI dropping to 52.9, which is the weakest level since May and down from July's 14-month peak of 55.8. The disappointing construction survey follows the weak manufacturing PMI report earlier in the week, together painting a picture of slowing economic expansion while highlighting the impact of Brexit uncertainty.

Developed market equities closed lower as trade tensions persisted and emerging markets remained under pressure. The S&P 500 index and the Euro Stoxx 600 index dropped -0.2% and -0.7% respectively.

It was a positive day of trading for regional equities. The ADX index and the Tadawul added +0.9% and +0.3% respectively. UNB closed limit up while ADCB added +12.8% as both banks confirmed reports that they are in talks for a potential three-way merger with Al Hilal Bank.

Oil prices traded in a wide range yesterday as the market absorbed the impact of a hurricane in the Gulf of Mexico. At one point Brent prices were up more than 2% and WTI gained even more. However, as news broke that Hurricane Gordon was moving away from the main oil and gas producing region prices fell and settled nearly unchanged on the day. This morning both Brent and WTI are trading lower.

Saudi Arabia is apparently targeting a range of USD 70-80/b for crude prices to balance the financing needs of the Kingdom and not dampen demand excessively. We would expect monthly production levels to be more responsive to prices if this price band is indeed Saudi Arabia’s objective but also that alternative producers will take this level as a signal to continue investment and production growth.

Forward curves and showing a diverging trend now that Brent has moved back into backwardation. The backwardation at the front end of the Brent curve has widened to nearly USD 0.3/b while in WTI it is trading around the same level after collapsing from over a USD 1/b spread in recent weeks. Longer dated spreads such as Dec 18/19 are showing the same story (wider in Brent and tighter to flat in WTI).

Click here to Download Full article