Recent Search

Popular Searches

Holidays in Japan make for a quiet start to the week which may help sentiment at least until US markets open. Markets ended last week in better shape than they spent much of it, but the possibility of more turmoil has not gone away with both fundamental and technical forces likely to continue exerting pressure. In particular, the passage of a US budget bill through Congress at the end of last week is only likely to reinforce the bullish bias to bond yields, given the impact it will have in boosting the fiscal deficit, possibly in excess of 5% of GDP.

The USD300bn two-year budget deal not only averted another government shutdown, but it has added significantly to upside growth and inflation risks in the coming year. The stimulus is worth approximately 0.5% of GDP, on top of the tax cuts already passed at the end of last year, making it likely that growth could exceed 2.5% in the U.S. in 2018.

After easing in December, the Emirates NBD Dubai Economy Tracker Index (DETI) rose to 56.0 in January mainly on the back of faster output and employment growth. The output/ business activity index rose sharply to 61.0 last month, the highest reading since July. The employment index rose to 52.3 in January, and while this does not indicate a staggering number of new jobs created, the reading is the strongest since November 2015

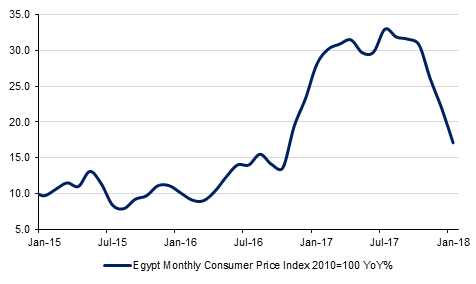

Egypt’s headline inflation rate fell from 21.9% y/y in December to 17.1% in January. This is the slowest rate since October 2016, just prior to the float of the Egyptian pound the following month. As the pound depreciated and inflation skyrocketed, the Central Bank of Egypt sharply tightened monetary policy, but with inflation falling once more we expect that the bank will cut rates at its upcoming monetary policy meeting on Thursday.

Source: Emirates NBD Research

Source: Emirates NBD Research

|

| Time | Cons |

| Time | Cons |

| India CPI y/y | 16.00 | 5.1% | US Monthly Budget Statement | 23:00 | $51.0b |

| India Industrial Production y/y | 16:00 | 6.1% |

|

|

|

Source: Bloomberg

It was a volatile week of trading for US treasuries amid risk-off mode in global equities. While short-end of the curve did benefit from safe-haven buying, the trend was more mixed on the long-end. Yields on the 2y USTs dropped -7 bps wow to 2.07%, rose +1 bp wow on 10y USTs to 2.85% and +7 bps wow on 30y USTs to 3.16%.

Regional bonds, followed moves in benchmark yields, and closed lower. The YTW on the Bloomberg Barclays GCC Credit and High Yield index jumped +11 bps wow to 4.07% and credit spreads widened 15 bps to 156 bps. The YTW has cross 4.0% for the first time since January 2016.

S&P affirmed Qatar’s long-term rating at AA- with negative outlook. The negative outlook reflects the geopolitical and economic risks from Qatar’s boycott by several GCC countries over the next 12 months.

The Dollar Index gained 1.30% last week to close at 90.44. During this consecutive week of gains, the index has risen back above the baseline that had originally held since September 2016. This indicates that we may be witnessing the start of a reversal. While the price remains above these levels, a test of 91.70 is likely to be the path of least resistance. At this level which sits at the 23.6% one year Fibonacci retracement and 50 day moving average (91.69), we expect the index to face stronger selling pressures and hence regard this to be the next level of resistance. On the other hand, a break below 88.90 would take the price back below the support baseline, voiding our view of a reversal and leading to more significant declines towards 85.

Regional equity markets, with the exception of the Qatar Exchange (+1.7%), started the week on a negative note. Weakness in oil prices over the weekend appeared to weigh on investor sentiment.

Dubai Investments closed flat even as the company reported weak earnings. However, the company announced plans to monetize its assets with an IPO of its cooling unit Emicool planned for Q4 2018 and listing of its real estate investment trust on Nasdaq Dubai or DFM.

Oil markets suffered their second consecutive weekly loss in a row last week, declining by nearly 10% in WTI and more than 8.4% in Brent. WTI closed the week below USD 60/b, its lowest level since the end of December while Brent was last below USD 63/b in early December 2017. The decline comes amid the continued sell-off in risk assets but bearish fundamentals from the oil market aren’t helping. US oil and gas explorers added 26 oil-focused rigs last week, the biggest weekly increase since January 2017. Investors also continued to pull out of long oil positions, cutting Brent and WTI longs by nearly 29k lots last week.

Market structures are holding roughly steady, despite the uptick in volatility in spot prices. The 1-2 month backwardation in WTI is holding at around USD 0.2/b while the similar time spread in Brent is stuck at around USD 0.3/b.