Recent Search

Popular Searches

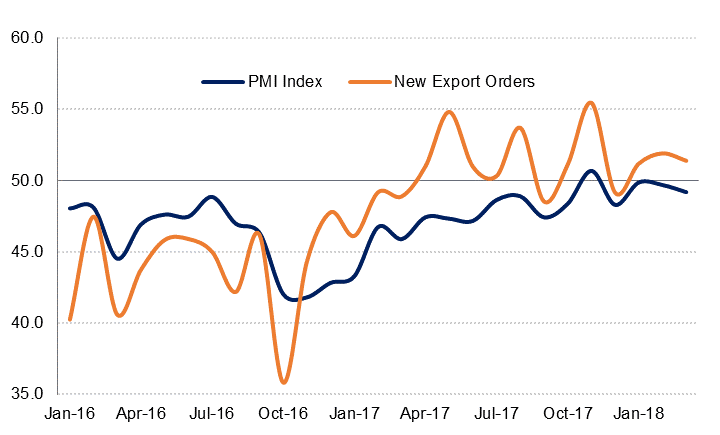

Emirates NBD’s Egypt Purchasing Managers’ Index (PMI) fell to 49.2 in March, from 49.7 in February. Having broached the neutral 50.0 level for the first time in two years in November, Egypt’s non-oil private sector has remained frustratingly just short of expansionary territory over the past several months. While we still anticipate an improvement in the Egyptian economy this year as the negative effects of its IMF-sponsored reforms pass through, the data implies that this is taking longer than the authorities might have hoped. Nevertheless, the index has consistently threatened to turn expansionary over recent months, which is a vast improvement on the months just prior to the onset of economic reforms.

Source: IHS Markit, Emirates NBD Research

One of the factors behind our expectation of improving conditions for the private sector in 2018 is a slowdown in inflation as the November 2016 currency devaluation has fed through. Headline CPI inflation has more-than halved since its peak of 33.0% y/y in July 2017, and this has been reflected in the PMI data, with the input price component falling to 61.0, its lowest level since September 2015. The fall in input purchase costs from 71.0 12 months ago to 61.2 in March is a major positive for firms that have struggled to pass all of their greater costs incurred onto customers, thereby squeezing their margins and their ability to invest.

On the positive side of the weaker currency, new export orders have consistently exceeded 50.0 in 2018 so far, coming in at 51.4 in March. New orders overall were at 50.0 in March. This is down modestly from 50.3 in February, but far above their 12 month average of 48.6, boding well for future output.

Looking ahead, business optimism towards future output in Egypt remains positive, but it is moderating. In March, only 43.7% of respondents expected that output will be greater in 12 months’ time – in December 2017 this number was at 70.0%. Those expecting that conditions will worsen remained low at just 3.0%, but more than half of respondents now believe that the rebound has run its course and output will remain at current levels. The subcomponent index reading was 70.3 in March, down from 80.0 the previous month and a 12-month average of 76.9.

Daniel Richards

Daniel Richards