Recent Search

Popular Searches

The Central Bank of Egypt (CBE) kept its benchmark interest rates on hold on at its April 28 meeting, with the overnight deposit rate at 8.25% and the overnight lending rate at 9.25%. This was the fourth consecutive meeting at which the central bank has held rates steady, despite persistently low inflation which has left its real rates among the highest in the world. We expected that the bank would remain on pause once more this time around, but once the potential inflationary pressures of Ramadan have faded, we see scope for one more rate cut to the tune of 50bps at the June 17 or August 5 meetings. The still resolutely dovish messaging from the US Federal Reserve, and resultant dip in USTs, should allow the CBE to cut rates once more without necessarily jeopardising international portfolio inflows, and potentially provide a modest fillip to growth. This will likely come through the government spending channel rather than private consumption, as lower interest rates will cut the debt servicing burden and make room for the greater projected public spending.

.jpg) Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

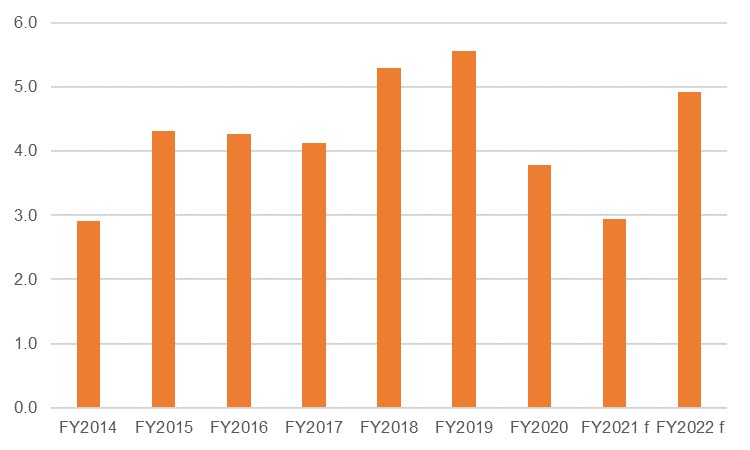

With the Covid-19 pandemic continuing to weigh on the Egyptian economy, both through the direct domestic channel and its wider global effects, we have downgraded our growth expectations. We now forecast real GDP growth of 2.9% this fiscal year (ending June 2021), followed by 4.9% next year. This compares to our more bullish previous expectation of 3.5% and 6.1%, when it looked like international travel might recover more rapidly than now appears likely. The Egyptian government is moderately more optimistic than our view, with a forecast of 3.3% this year and 5.4% next year, and indeed it will be the government that will be the primary growth driver as it has signalled a significant ramp-up in investment.

The outlook for Egypt’s tourism sector remains uncertain in the near term given that the Covid-19 pandemic is far from over, with some major economies seeing rapidly surging cases in recent weeks. Even as key source markets for visitors to Egypt such as the UK, and (more belatedly) some major Eurozone economies make strong progress with domestic vaccination programmes, fear of new variants of the disease will see a slow easing of restrictions on international travel. As such, the sector will not only remain a drag on output through the remainder of this fiscal year, but it looks increasingly likely that it will continue to exert pressure through the start of the next fiscal year also. There has been some positive news for the sector, as Russia has agreed to resume all flights to Egypt – suspended following the bombing of a Russian tourist flight in 2015 – but it is unclear when this will begin and is unlikely to herald an immediate return of all visitors. In any case, Egypt received just 500,000 tourists over the January-March, compared to 2.4mn in the same period in 2018. A poorly performing tourism sector weighs on the Egyptian economy through a variety of channels aside from exports, with investment and private consumption also directly affected.

Source: Haver Analytics, Emirates NBD Research

Source: Haver Analytics, Emirates NBD Research

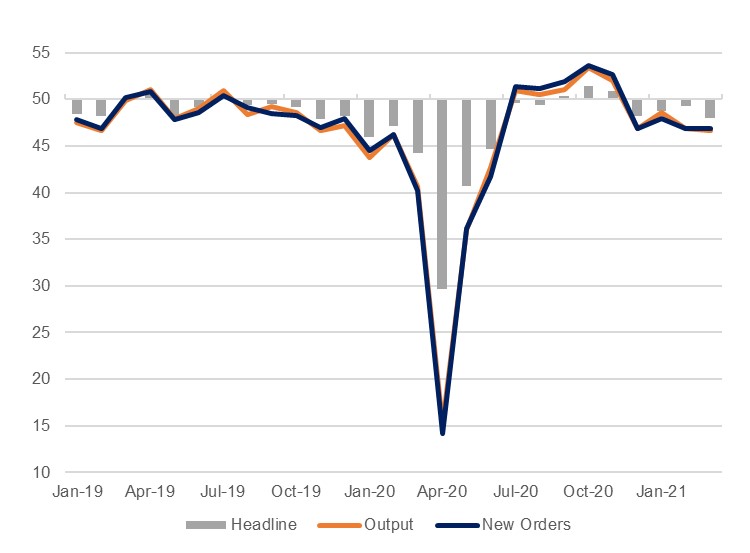

Aside from tourism, the private sector more generally remains under pressure, and has deteriorated in recent months according to the PMI survey which slipped to a nine-month low of 48.0 in March, the fourth-consecutive sub-50.0 reading. This was the lowest reading since the recovery from the initial Covid-19 slump began last year and reflects the pressures that the virus continues to exert, not only domestically but also in terms of Egypt’s trade partners. New export orders fell at the fastest pace since May last year, in sharp contrast to the record expansion seen the previous month. New domestic orders were also soft, with total new orders contracting for the fourth month in a row. We would share the respondents’ view that the outlook is for an improvement hereon in – future expectations were at their highest level since last July, and only 1% of surveyed firms expected that things would get worse – but over the next several months at least global dynamics will continue to provide headwinds to growth.

Source: IHS Markit, Emirates NBD Research

Source: IHS Markit, Emirates NBD Research

In this environment, announcements by the Egyptian government with regards boosting spending are a positive for GDP growth. As has been the case for much of the five years since the economic reform programme began, public investment will be a key driver of economic expansion, bolstered by plans announced by minister of planning and economic development Hala al-Saeed to target EGP 1.3tn in total investments. Of this, EGP 358bn will be spent on 12,000 individual projects around the country. Foreign direct investment into Egypt fell -9.5% last fiscal year in nominal terms and is unlikely to see a rapid pick-up over this year or next given the ongoing global issues. As such, the government’s signal that it is looking to pick up the slack will help keep Egypt one of the global outperformers when it comes to growth. It was one of the few economies globally to record an economic expansion last year.

Daniel Richards

Daniel Richards