Recent Search

Popular Searches

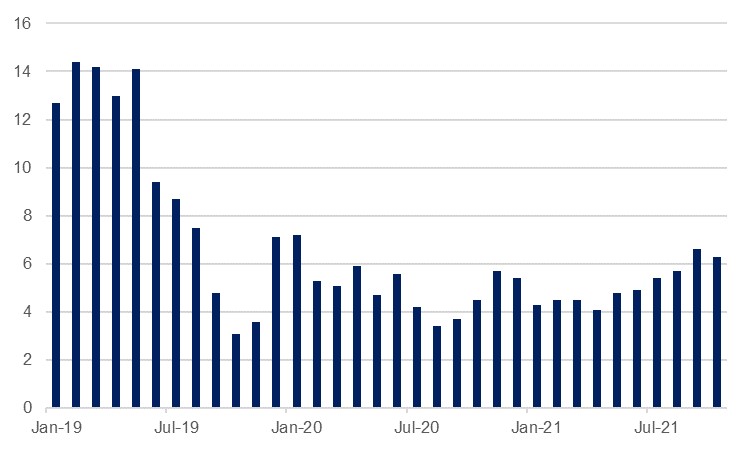

Egypt’s urban CPI inflation print came in at 6.3% y/y in October, slightly faster than we anticipated but still lower from the 6.6% recorded the previous month. On a monthly basis, price growth was 1.5%, an acceleration from the 1.1% recorded in September and the fastest pace since October 2020. Food price inflation continues to accelerate on the back of unfavourable base effects, rising from 10.6% y/y in September to 11.6% last month, while education has also been a notable driver of price growth, offset in part by other nonfood components of the basket for which inflation has been moderating.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Successive PMI surveys for Egypt have highlighted the stresses businesses are experiencing from the global supply chain issues as higher costs for shipping and raw materials, alongside rising wages, saw firms’ input prices rise at the fastest pace in three years in October according to the latest survey, and these costs are increasingly being passed on to the consumer. As sectors such as tourism continue to recover from the pandemic crisis, domestic demand is also likely to accelerate, and we project an average CPI inflation rate of 6.3% next year. This is below the consensus projections of 6.6% given our expectation for some of the energy pressures to ease and supply chain issues to begin to alleviate, but it would still mark the fastest pace of price growth since 2019.

Given these expectations, we expect no more rate cuts by the Central Bank of Egypt during this cycle, with the next move more likely to be a leg higher; we are projecting a 25bps hike in Q1 2022, with a second in the third quarter taking the year-end overnight deposit rate to 8.75%. Our inflation projections are well within the CBE’s target range of 7 percent (±2 percentage points) on average in 2022 Q4, and real rates are expected to maintain a healthy margin compared to many peers. Nevertheless, with global monetary tightening on the horizon, the central bank will likely be keen to ensure this through raising rates in line with trend price growth. This will help preserve interest in Egyptian debt even as yields on USTs rise ahead of anticipated hikes by the Federal Reserve; foreign ownership of Egyptian debt picked up to a record USD 24.1bn in September.

.jpg) Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

A steady recovery by the tourism sector over the next 12 months, alongside increased FX inflows from the Suez Canal (the authority has recently hiked rates for all vessels save cruise ships and gas carriers passing through the waterway, which has been particularly busy lately with a new record of 87 transit vessels one day in September) would help offset any potential fall in portfolio investment that could materialise as global policy tightens. As such we expect any pressures on the EGP to be relatively manageable, projecting a depreciation to EGP 16.00/USD by end next year, from the present EGP 15.71/USD. On a REER basis the currency has been trading above both its 10- and 20-year averages over the past two years, but the authorities will be wary of any sharp moves lower that might accelerate inflation, impede the recovery, and negatively impact lower-income households.

Daniel Richards

Daniel Richards