The common take away regionally and globally is how economic performances have largely defied political risks and uncertainties in 2017. This provides grounds for optimism even though the world economy and our region will continue to face significant challenges next year.

- Global macro: This year has been an astonishing one in many respects, with global growth largely defying the doomsayers despite an increasing incidence of political and geopolitical risks.

- GCC macro: November has been a month of heighted political uncertainty and financial market volatility in the GCC. However, the economic fundamentals are constructive as we head into 2018.

- MENA macro: The outlook for North African energy importers is brighter.

- Sector focus: UAE’s wholesale & retail trade sector overview.

- Emerging market focus: India

- Interest rates: Relentless demand for longer dated treasuries continue to flatten the UST curve amid solidifying expectations of one rate hike in December this year and further two to three in 2018.

- Currencies: Constructive data and receding political risks have aided the Euro in outperforming rival G-10 currencies over the last month. These gains have resulted in the single currency being the best performer year to date in 2017.

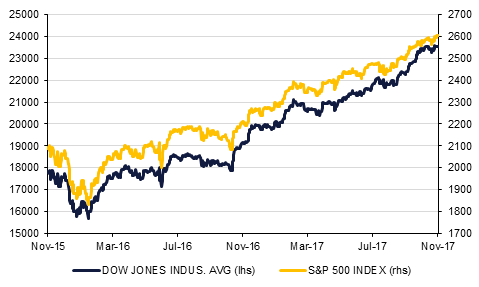

- Equities: 2017 has been a phenomenal year for global equities with all major indices trading at new all-time highs. With geopolitical risks largely contained and factors behind the move in 2017 still firmly in place, a reasonably confident argument for continuation of risk-on stance in 2018 can be made.

- Commodities: We are revising higher our oil price assumptions for 2018 even as we expect to see some challenging fundamentals from non-OPEC supply growth next year. Political risk will come back into play even if we see no direct risk to output.

"Trumpflation" remains alive as year-end approaches

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Click here to Download Full article