Recent Search

Popular Searches

ECB President Christine Lagarde said on Wednesday that the European Central Bank will focus on more emergency bond purchases and cheap loans for banks when it puts together its new stimulus package next month to help the Covid-19-hit Eurozone economy. Lagarde said inflation in the 19-country bloc was now likely to remain negative for longer than expected as a second wave of the pandemic places new restrictions on economic activity. Lagarde said that the ECB's job was to keep borrowing costs low enough for households, firms and governments and to support the banking sector to prevent a credit crunch. She muted excitement over Pfizer’s vaccine saying that recurring cycles of accelerating viral spread and tightening restrictions are still likely until widespread immunity is achieved.

Irish Foreign Minister Simon Coveney said an EU-UK trade pact is unlikely to come together this week and negotiations might go into the next. The latest agenda expected ratification by the plenary on December 16 if the lawmakers got a text ready by Nov.16. The EU parliament has already warned time was running out to put in place any new trade agreement, which must still be approved by the 27 national EU leaders, who are next due to come together on November 19 in a video call amidst Covid-19 restrictions, as well as the European Parliament. Britain’s status quo transition period expires at the end of the year, and talks on trade rules that would apply from the start of 2021 have yet to yield a breakthrough. The government has also stepped up regular talks with UK industry groups to try and minimise disruption when the transition period ends.

The German Council of Economic Experts (GCEE) said on Wednesday the German economy will shrink by a less than initially feared -5.1% this year thanks to a strong rebound over the summer. This would be a similar contraction to that seen during the 2009 financial crisis. The GCEE anticipates a relatively slow recovery of 3.7% in 2021 and said it was unlikely that the pre-crisis level of output would be achieved before early 2022. Euro-area GDP is expected to contract -7.0% this year, before rebounding 4.9% in 2021, although the report notes that risks are skewed to the downside.

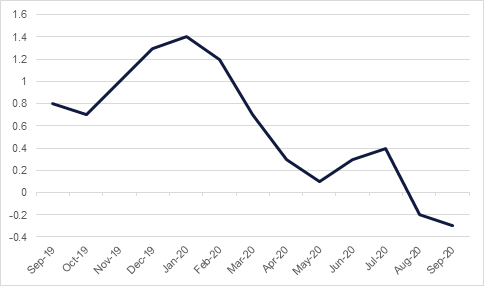

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

US cash markets were closed thanks to a public holiday but USTs have opened higher in early trade today. Yields on the 2yr note have dipped slightly to 0.1787% while on the 10yr they have fallen to 0.9360%.

Fitch rated the UAE at ‘AA-‘, the first nation-wide sovereign rating. The rating agency noted that the UAE is considering issuing nation-level bonds in order to build out a sovereign yield curve. Fitch estimated UAE federal government debt at just 0.7% of GDP while consolidated emirate-level debt is estimated at 34% with a wide variance by individual emirate.

Following outlook revisions on the Saudi Arabia sovereign and Aramco, Fitch also revised its outlook on Sabic to negative while affirming the chemicals company rating at ‘A’.

The USD strengthened on Wednesday as optimism surrounding a coronavirus vaccine keeps running high. The DXY index earned modest gains and sits just below the 93 handle. USDJPY fluctuated between the 105 – 106 big figures but is unchanged this morning at 105.30.

The EUR dipped from early highs of 1.1833 to lows of 1.1746 after some dovish comments form ECB members and currently trades at 1.1780. The GBP dropped to 1.32 amid reports that Brexit talks will run past the November 15th informal deadline and remains just above that figure this morning. The NZD continues its positive form, rising to a 19-month high of 0.6915 after upbeat comments from the RBNZ and trades around 0.6890.

Despite cautious words from Christine Lagarde, and the ongoing hurdles presented by EU-UK trade talks, European equity markets continued to rise on the back of vaccine-related optimism yesterday. In the UK, the FTSE 100 rose 1.4% to a five-month high, while France’s CAC (0.5%) and Germany’s DAX (0.4%) also gained. In the US it was the tech-heavy NASDAQ’s turn to outperform after it was the one of the three major indices to decline on the back of the Pfizer news earlier in the week. It gained 2.0%, while the S&P 500 rose 0.8% and the Dow Jones lost -0.1%.

In Asia, the Shanghai Composite closed down -0.5% yesterday, and is trading -0.2% lower this morning. A Chinese government crackdown on its internet giants has impacted tech shares.

Oil prices extended their gains for a third day running overnight and have kept rising in early trade today. Brent futures settled up at USD 43.80/b, a gain of 0.4%, while WTI was up 0.2% at 41.45/b. Market chatter remains fixated on whether OPEC+ will delay its production increase scheduled for the start of the year with policymakers reportedly considering a delay of three to six months before increasing output.