Recent Search

Popular Searches

Politics remained at the forefront of investor concerns. Ahead of the formal start of trade talks between the US and China, comments from Chinese officials highlighted the challenges that lie ahead. A Chinese foreign ministry official in response to questions over blacklisting of technological firms indicated a retaliation in some form and asked to ‘stay tuned’. More strong words were used by Chinese officials later in the day when the US introduced visa bans on some Chinese officials.

On the Brexit front, the UK Prime Minister Boris Johnson told German Chancellor Angela Merkel that a deal is essentially ‘impossible’ if the EU insists that Northern Ireland remains in the customs union. He also lamented EU’s unwillingness to engage with his new proposals. In response, some EU leaders asked the UK Prime Minister not to try and win the ‘blame game’.

Beyond politics, economic data continue to remain subdued. The US Produce Price Index dropped -0.3% m/m indicating that inflationary pressures at the moment remains negilible. Interestingly, core goods prices fell 0.1% m/m despite introduction of tariffs on Chinese goods at the start of the previous month. In the Eurozone, German industrial production data surprised positively as it rose 0.3% m/m compared to consensus expectation of no change. However, on a y/y basis, the data showed a drop of -4.0%, a slight improvement to previous month’s reading of -4.2% y/y.

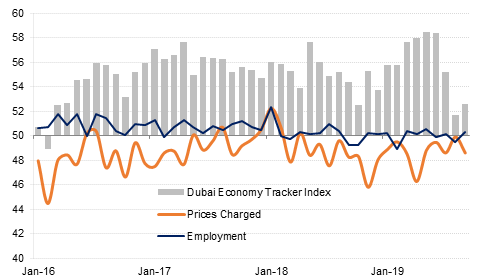

The Dubai PMI rose slightly to 52.6 in September, but the average reading for the third quarter was the lowest since Q1 2016. This signals a slower rate of growth than the survey data pointed to in H1 2019. There was a marked deceleration in new order growth in Q3, with the September reading for this component the lowest since February 2016. Further price discounting, particularly in the wholesale & retail trade sector, likely contributed to a pick up in output growth last month. However, the survey suggests that on average there was no growth in private sector employment in Dubai Q3 2019.

Source: Emirates NBD Research, IHS Markit

Source: Emirates NBD Research, IHS Markit

Treasuries traded higher as optimism over trade talks between the US and China faded away. The curve shifted lower with yields on the 2y UST, 5y UST and 10y UST closing at 1.41% (-5 bps), 1.35% (-4 bps) and 1.52% (-3 bps) respectively.

Ahead of the release of the last Fed meeting, Jerome Powell said that the Federal Reserve will resume purchase of Treasury securities to avoid a repeat of wha happened in repo market last month. The Chairman said that the measures are not a return to the QE program but that they relate to the recent ‘technical issues’. He did not comment on the size of the purchase.

Regionl bonds continue to trade in a tight range as investors remain conscious of the flurry of new issuances in the pipeline. The YTW on Bloomberg Barclays GCC Credit and High Yield index was at 3.23% while credit spreads widened slightly to 173 bps.

Despite a decline in consumer confidence, AUDUSD is trading firmer this morning. A survey from Westpac showed that consumer confidence declined 5.5% m/n in October, following a 1.7% decline the previous month. As we go to print, AUDUSD is trading 0.21% higher at 0.67423. We expect the first level of resistance to be at 0.6780, not far from the 50-day moving average (0.6779).

Developed market equities closed lower as tensions between the US and China escalated ahead of the formal start to the trade talks. The S&P 500 index and the Euro Stoxx 600 index dropped -1.6% and -1.1% respectively.

Regional equities were unable to hold onto gains of yesterday’s session. The Tadawul and the DFM index dropped -0.6% and -0.2% respectively. Across indices, banking sector stocks came under pressure with Al Rajhi Bank, Dubai Islamic Bank and First Abu Dhabi Bank declining -1.3%, -0.8% and -0.4% respectively.

Oil markets extended their losses overnight, falling by around 0.2% in both Brent and WTI futures. Both contracts are trending lower this morning with WTI at USD 52.43/b and Brent and USD 58/b. The EIA revised higher its forecast for US crude oil production growth this year to 1.27m b/d from 1.25m b/d in its previous forecast. Its outlook for 2020 production was revised lower but at an average production of 13.17m b/d the US will still be the largest single producer of crude in the world. The EIA also cut back its global demand projections for 2020 to growth of 1.3m b/d and expects demand this year to come out at 840k b/d.

Crude inventories in the US rose by over 4m bbl last week according to data from the API. Official inventory data will be released later this evening from the EIA.

Edward Bell

Edward Bell