Recent Search

Popular Searches

UK inflation data for January will be the main economic release today, with the headline rate expected to remain at 3.0% still some 1.0% higher than the Bank of England’s 2.0% target. This would of course be uncomfortable for the Bank and would help to explain its change of tune last week when it turned more hawkish. The Bank indicated in its Inflation Report that it is less inclined to tolerate inflation above target over the next three years, bringing the prospect of a May rate hike on to the stage, with a further hike in the second half of the year also looking likely.

The economic data releases from India yesterday painted a relatively positive picture. The CPI in January rose 5.07% y/y, in line with estimates of 5.10% but lower than 5.21% y/y increase in December. Industrial Production data showed an uptick of 7.1% y/y in December 2017, higher than estimates of +6.0%. The ease in inflation should come as a relief for investors given the concern expressed by the Reserve Bank of India at its last meeting. The data released supports our view that the RBI is likely to keep interest rates on hold at least until H1 2018.

Donald Trump unveiled his administrations USD200bn infrastructure plan yesterday, with the hope that along with local, state and private investment it will reach a total of USD1.5-1.7 trillion in new spending over ten years. That is the theory, but how such financing will be achieved in practise is unclear, and for this reason there are already significant doubts about whether any of the plans outlined will be accomplished beyond the Federal government’s initial USD200bn outlay, which will it self not be easy to find given the ballooning budget deficit. The infrastructure allocation came as part of the overall USD4.4 trillion budget proposal which abandons the long-held Republican Party objective of balancing the federal budget within a decade.

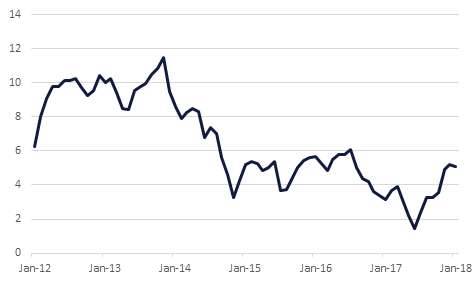

Yields on 10yr USTs continued to move ever higher yesterday, closing at 2.855%, up 2bps and are still pushing higher this morning. Beyond the volatility that began in equity markets hitting all asset classes, the US treasury market is weighing up major stimulus packages in the US and the impending sizeable increase in the deficit that will be a result. The move up in yields was mirrored across the Atlantic with bund yields up while gilts were roughly flat.

With benchmark markets still choppy we would expect the new issue supply to be limited from the region at this stage.

NZD underperformed on Monday, losing ground against the other major currencies. These losses were despite reports from Statistics New Zealand which showed health spending in January. Retail card spending increased to 1.4% m/m, up from 0.6% m/m and beating expectations for a 0.4% increase, while total card spending accelerated to 0.6% m/m from 0.2% m/m. In the aftermath of the reports, NZDUSD found support and gained before encountering resistance near the 61.8% one year Fibonacci retracement.

This afternoon, investors will be turning their attention towards the UK where economic data is expected to show that heading consumer prices increased by 2.9% y/y in January. With the Bank of England last week highlighting that higher interest rates may be required sooner than initially anticipated, any upside surprise in the data is likely to be supportive of sterling.

Global equities built on the positive momentum from the end of the last week. All major equity indices rallied ahead of the inflation data in the US on Wednesday. The S&P 500 index added +1.4% and the Euro Stoxx 50 index gained +1.3%.

Regional equities were largely positive. The Tadawul added +1.3% on the back of strength in market heavyweights. Al Rajhi Bank added +2.0% and Sabic gained +1.3%.

Elsewhere, Air Arabia rallied +0.8% after the company announced better than expected earnings for 2017 and announced an increase in dividends.

Oil markets licked their wounds to start the week, holding roughly flat on where they ended last week. WTI rose by 0.15% to close at USD 59.29/b while Brent was slightly down to close at USD 62.59/b. In its latest oil market assessment, OPEC revised higher its demand expectations for 2018 but also revised upward its forecast for non-OPEC supply growth this year. OPEC projects that the market would only return to balance at the end of the year, later even than our own forecasts. As a counterpoint to OPEC’s projections, the EIA estimates that oil supply from shale basins in the US will increase by 111k b/d month on month in March, an acceleration from the 109k b/d expected this month.