Recent Search

Popular Searches

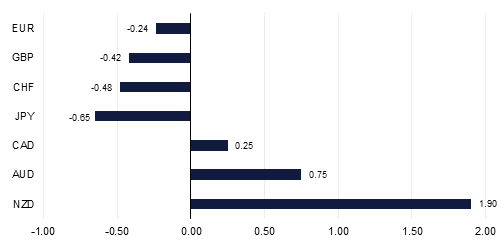

The dollar is continuing to benefit from recent events, even as the Fed has adopted a more dovish posture. The dollar is largely a beneficiary by default as the situation in a number of other economies is becoming of greater concern than that in the United States. Germany only just avoided a recession at the end of 2018, and political risks are rising across the Eurozone with Spain becoming the latest to come into the spotlight, calling a snap general election on April 28th. Elsewhere Brexit continues to dog sterling, with the impression increasing that this will not be resolved until the final week of March, just before the UK is due to leave the EU.

Meanwhile, US-China trade talks last week failed to achieve an agreement, although they are due to resume in Washington this week, as both parties acknowledged making some progress. However, some very difficult issues remain including structural reforms and intellectual property theft. President Trump also signed the border security funding bill that averted another government shutdown, although in the process he also declared a national emergency, which will likely trigger lengthy court battles. On the positive side monetary policy has turned supportive with the FOMC now advocating patience, and the ECB contemplating new TLTROS. This week's focus will be on the FOMC minutes to the January policy meeting as we look to gain more information on the Fed's switch to a more dovish stance. There will also be a large number of speakers from the ECB, with the market looking for confirmation that they are also looking at loosening policy again. Not only is the Eurozone struggling with growth, but there is again speculation that it may also be the next in line when it comes to facing US trade tariffs.

For the UK the next key event is February 27, when parliament will vote on the government's Brexit plan again, leaving the upcoming week in a kind of limbo, except for the monthly labour market data. Even here though with the Bank of England essentially in wait and see mode it will have to be strikingly different from the consensus to elicit any significant response from GBP.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg