Recent Search

Popular Searches

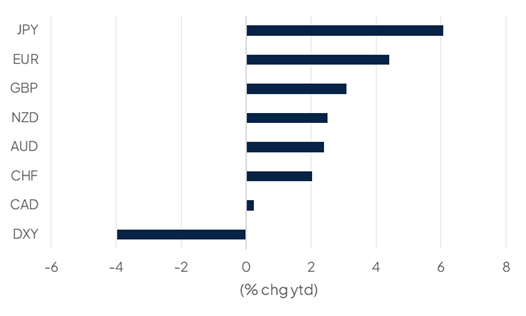

The US dollar index has slumped in 2025 as anxiety over the negative impact of tariffs on the US economy pairs with reinvigorated spending plans from Germany, Europe’s largest economy, to shift the outlook for the dollar and US rates. The DXY index, which is heavily weighted toward the Euro, fell to 104.3 by 5 March 2025, down 3.9% since the start of the year and is close to erasing all the gains accrued since US President Donald Trump was re-elected.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

At the end of last year, expectations that many of the Trump administration’s policies—tariffs, a crackdown on immigration, tax cuts—would fuel inflation fed into projections that the Federal Reserve would be limited in how much it could cut interest rates in 2025, following 100bps of easing in H2 2024. At the same time the outlook for Europe’s economy remained weak and apparently in need of additional cuts from the European Central Bank. That supported a widely held view, including on our part, of a strong US dollar/higher US rates relative to peers.

But market focus has now turned to the negative economic consequences of President Trump’s tariff and other policies, with the president himself noting during his congressional address in early March that tariffs would cause “a little disturbance.” Expectations for a US recession this year have crept higher in recent weeks while the Atlanta Fed’s nowcast of GDP has shifted from expansion of more than 2% as of late February to a contraction of 2.8% q/q annualized in its most recent estimate.

There have been signs of the US economy cooling—the ISM manufacturing print for February was in particular disappointing—but not yet flashing red from other signals. Employment remains in good shape and the February nonfarm payrolls report is expected to improve to around 160k, up from 143k in the initial January estimate. Inflation also remains a challenge for the US, having cooled substantially over the last several years but remaining above the Federal Reserve’s 2% target level.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

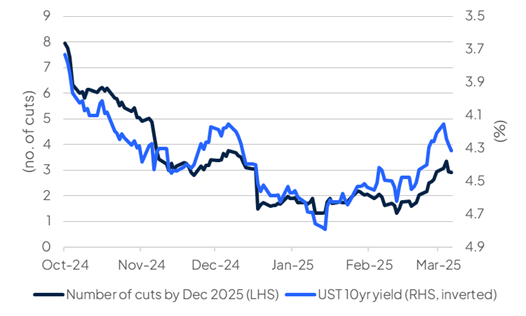

Pricing for where the Federal Reserve will take rates this year has also shifted. Only as recently as mid-February barely one more 25bps cut was being priced in for this year as markets did not expect that tariffs would be applied to Mexico and Canada and that the threat of tariffs against the EU or other US trading partners would remain only threats. Now that tariffs have been imposed and been met with retaliation, market pricing has shifted to more rate cuts this year, hitting a high of 83bps of cuts by December 2025 as of the start of March.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

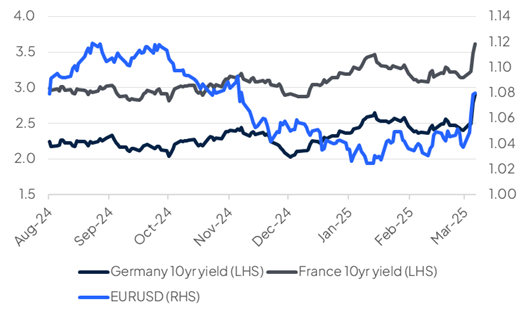

At the same time the incoming German chancellor, Friedrich Merz, is poised to spend heavily on defence and infrastructure in Europe’s largest economy to try and reverse a lengthy period of economic drift and to build up domestic defence capabilities. German 10yr bund yields have spiked in response, taking the rest of Eurozone bonds with them. The European Central Bank is poised to cut rates again on March 6 2025 but with a renewed fiscal impulse on the verge of taking hold in the Eurozone, the outlook for where Euro rates will go now hangs in the air. Taking the path of least resistance, EURUSD has surged and moved well away, in the near term at least, from the risk of hitting parity.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

A reinvigorated German economy would certainly be welcome for global demand and a weaker dollar, if it persists, can take some of the sting of tariffs out of the cost of global trade. As the outlook for Euro rates grows clearer and if there are fewer barriers than anticipated to the incoming German government’s spending plans, we will revaluate our expectation for the Euro accordingly.

Edward Bell

Edward Bell