Recent Search

Popular Searches

Markets were relatively quiet thanks to a public holiday in the US to start the week. A new round of US-China trade talks will begin today in Washington and the relatively positive end of talks last week should continue to buoy risk sentiment.

Business confidence in Japan weakened this month to the lowest levels since the end of 2016 as global trade issues take their toll on the economy. The Reuters Tankan index fell in both the manufacturing and services sector with retailers among the least optimistic about the outlook for 2019.

Saudi Arabia has signed memorandums of understanding worth USD 20bn covering investments into Pakistan on the occasion of crown prince Mohammed bin Salman’s visit to the country. Pakistan is facing external payments pressure and foreign exchange reserves have dipped to just two months of import cover. The investments are still very much on paper at this stage and a plan to build a new oil refinery at the port of Gwadar will take years to materialize. Saudi Arabia had recently provided Pakistan with a USD 6bn loan to help build up forex reserves and give the country time to negotiate assistance with the IMF.

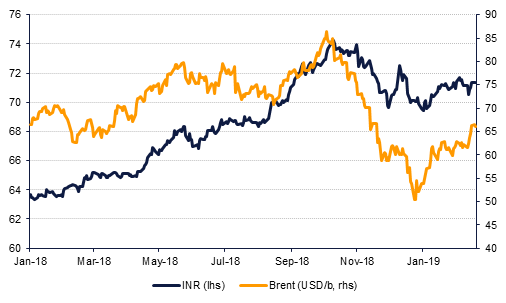

The Indian rupee has spent the past few days on the back foot and has now moved back above 71 rupees to the dollar. A few factors are at play here in contributing to a weaker currency. One is India’s upcoming elections in a few months’ time and what that means for fiscal policy going forward. Our view is that any deficit that emerges as a result of higher government spending will be manageable and won’t place undue pressure on fiscal balances. From the external side, India’s external accounts are heavily impacted by moves in international oil prices. India is large net importer of crude oil and the country has among the strongest levels of demand growth globally. With oil prices hitting their 2019 highs, markets will grow worried about the pressure higher import costs will place on India’s external balances.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

US Treasuries had a range-bound day amid the US holiday. Yields on 2y, 5y and 10y USTs closed at 2.51%, 2.49% and 2.66% respectively, largely unchanged from their opening levels. Risk-on sentiment left CDS levels on US IG and Euro Main a little lower at 63bps (-2bps) and 68 bps(-1bp) respectively.

GCC bonds had no material catalyst for change with average yield on Barclays GCC bond index closing unchanged at 4.34% and credit spreads only a touch tighter at 180bps.

S&P downgraded DAMAC’s rating by a notch from BB to BB-, citing expectation of continued weakness in the Dubai real estate market. Nevertheless, after bottoming out at $86.74 in end January, DAMAC 23s have recovered to $88.54 (YTW of 10.06%)

Saudi Arabia's Finance Ministry yesterday issued 9.376 billion riyals ($2.50 billion) in domestic sukuk, under its monthly issuance program for February. As per the statement released by the ministry, it issued 1.805 billion riyals worth of five-year bonds, 0.274 billion riyals in 10-year bonds, and 7.297 billion riyals in 12-year bonds.

The AUD is trading softer in the aftermath of the RBA minutes and is currently on target to decline for a second day, having found resistance at the 100-day moving average (0.7160) on Monday to fall at the start of the week. As we go to print, AUDUSD is trading 0.30% lower at 0.7109, and is back below the resistive 50-day moving average (0.7135). While the price remains below the 100-day moving average, the risk is that we see further declines towards the 23.6% one-year Fibonacci retracement of 0.7023.

Elsewhere, GBPUSD is trading 0.18% lower and looks primed to retest the 100-day moving average (1.2875). Should it break this level, a further descent towards the 50-day moving average (1.2836) cannot be ruled out. The threat of this scenario will increase substantially should this afternoon’s UK employment data disappoint market expectations.

Investors’ optimism remained high despite no new development on the US-China trade talks, leading most stock indices in the developed world higher yesterday. S&P 500 and Dow Jones were up over 1% and Euro Stoxx inched up by 0.11%. Asian indices are also trailing in the green this morning with Nikkei and Hang Seng up +0.09% and 0.05% respectively in early morning trades.

Regional equities had a mixed day. DFM closed higher though Abu Dhabi index closed a tad weaker on the back of continued weakness in real estate sector. Tadawul lost -0.3% and Qatar index was largely unchanged.

Brent futures extended their gains overnight, rising five days in row to a new 2019 high of USD 66.50/b at the close and at one point were within distance of USD 67/b. With the US out for a public holiday there was no close for WTI.

The outcome of US-China trade talks remains paramount to the near-term outlook for oil prices. Negotiations have so far remained positive although an official extension of the deadline of early March has not yet been declared by the US.

Edward Bell

Edward Bell