Recent Search

Popular Searches

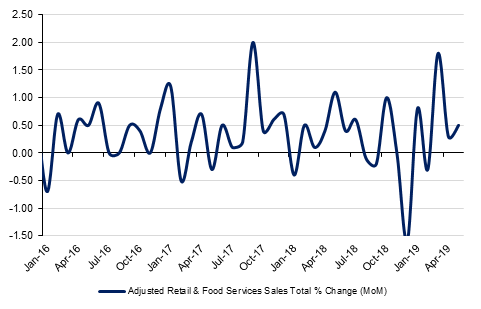

US retail sales and industrial production data put a dent in hopes for a Fed easing this week, with stronger than expected increases of 0.5% and 0.4% respectively, combined with upwards sales revisions for previous months. Consumer confidence data admittedly fell back a little in June, probably reflecting some anxiety about ongoing trade tensions. Prior to the data markets had a 90% probability of a rate cut at or before the July FOMC meeting built in, but this has since fallen back slightly to 85%. That still looks too high from our perspective and while a rate cut this week seems highly unlikely we think that the Fed will probably sit out the summer before making a decision of whether to ease policy in September, once more data has been accumulated.

Nonetheless the upcoming FOMC meeting on Tuesday and Wednesday this week will likely show the Fed becoming more dovish, with the new dot plot projections expected to show no change in the target rate in either 2019 or 2020, versus a prior assumption of a quarter point hike in 2020.

Meanwhile geopolitical risks returned at the end of last week with the news that two tankers were damaged in the Gulf of Oman, just outside of the Strait of Hormuz, causing oil prices to rise after spending the early part of the week under pressure. Trade tensions are also continuing to build this time between India and the US with India saying over the weekend that it will impose tariffs on 28 US products, some as high as 70%, in response to the US refusal to exmpt India from higher taxes on steel and alummium imports.

Finally two sets of data released released over the weekend showed the Dubai economy picking up. The headline Dubai Economy Tracker (DET) Index rose to 58.5 in May, the highest reading since January 2015 on the back of strong growth in output and new orders. Separately the Department of Economic Development (DED) published its Business Confidence Index which climbed to 117.8 points in Q1 2019 from 116.4 points a year ago.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

It was a week of two halves for Treasuries last week. While the first half saw investors lock in their gains, the second half was dominated by return of safe haven buying amid escalating geopolitical tensions. Yields on 2y, 5y and 10y USTs ended the week at 1.84% (flat w-o-w), 1.83% (-2bps w-o-w) and 2.08% (flat w-o-w) respectively. Sovereign bonds across the pond were a bit mixed with yield on 10yr Gilts increasing 1bp to 0.84% while those on 10yr Bunds declined 4bps to -0.26%.

Regionally, GCC Bonds closed largely unchanged with yield in Bloomberg Barclays GCC index remaining stable at around 3.73% and credit spreads at around 174 bps. Amid the rising political concerns in the region, demand for credit protection increased, pushing GCC sovereign CDS spreads higher. Spread on 5yr CDS on Saudi Arabia closed at 88bps (+3bps, w/w), on Qatar at 67bps (+2bps), on Abu Dhabi at 62bps (+1bp) and Dubai at 141bps (+6bps).

A 1.11% decline over the last week took EURUSD down to 1.1209, cancelling most of the gains of the previous week. Technical analysis of the daily and weekly candle charts show some interesting developments over the last week. For a second week, resistance was found at the 200-week moving average (1.1347) which put a cap on gains. In addition, the declines on Friday saw the price break below both the 100-day moving average (1.1270) and 50-day moving average (1.1219). While the price remains below this level, there is a risk of a retest of the 2019 low of 1.1107.

USDJPY rose for the first time in four weeks, rising 0.34% to close a 108.56. However, despite these gains, USDJPY was unable to break back above the 38.2% one year Fibonacci retracement (108.57) and remains vulnerable to declines while the price continues to close below this level on a daily basis.

GBPUSD fell last week, paring the previous week’s gains with a 0.66% decline that took the price to 1.2589. On Friday, support at the 23.6% Fibonacci retracement (1.2663), which had prevented losses earlier in the week, was shattered. This is very bearish for the price and a slide towards 1.25 cannot be ruled out in the week ahead. The risk of this is further augmented by the 14-day Relative Strength Index (RSI) which is at 33.88 and bearish in momentum.

Regional markets started the week on a negative note as investors locked in recent gains amid geopolitical tensions.The DFM index and the Qatar Exchange lost -0.7% and -0.3% respectively.

In an interview the Saudi Arabia’s Crown Prince Mohammed Bin Salman said that Aramco can go through an IPO as soon as next year. He added that no decision has been made on where the stock will list.

Oil markets were wrenched by competing forces last week as anxiety over global demand conditions weighed on prices to start trading while elevated geopolitical tensions boosted prices toward the close. While prices did surge on news that two tankers were damaged in the Gulf of Oman, just outside of the Strait of Hormuz, benchmark futures closed the week lower at USD 62.01/b for Brent (down 2% over the week) and at USD 52.51/b for WTI, down 2.7%.

Forward curves in both Brent and WTI suggest to us that the fear of a trade war cratering oil demand still remains the dominant risk for the rest of the year. Front month backwardated spreads in Brent gained on news of the tanker attacks but still closed the week lower while the contango in WTI deepened (another build in US crude inventories highlights the relative oversupply in US vs international oil balances). Longer dated spreads look particularly vulnerable to trade war risks. Brent Dec spreads for 20/21 are almost in contango, having fallen from almost USD 3/b in May to barely above neutral now.

Click here to Download Full article