Recent Search

Popular Searches

Markets responded positively to news that US president Donald Trump may extend the deadline for US-China trade talks after a visit of senior US officials to Beijing last week. Talks are set to resume in the US this week and Chinese media has reported that both sides had reached “consensus in principle” on several topics. However, there is still substantial difference on how any agreement will be implemented and enforced. The necessity of a trade deal is growing all the more apparent given a string of softer data coming out of both the US and Chinese economies.

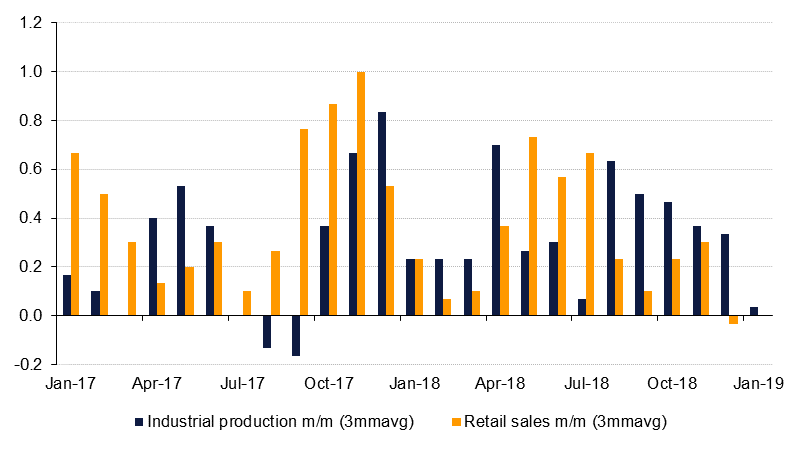

The US economy had been the standout performer compared with the Eurozone, China or Japan but signs of waning growth are starting to appear with more regularity. Retail sales in December fell 1.2% month/month in December, far off market expectations of what should normally be a good month helped by holiday purchases. In January, industrial production fell by 0.6% m/m thanks to a large degree by a nearly 9% m/m drop in vehicle manufacturing. Several Fed officials said over the weekend they were leaning to only one more rate hike this year (Atlanta and Philadelphia Fed presidents) while the San Francisco Fed president, Mary Daly, indicated that no hike may be needed at all.

President Trump has also declared a national emergency in order to appropriate funding for his US-Mexico border wall project. The US government funding bill signed last week did not include direct funding for the wall so the president has resorted to emergency action that will see funds taken away from other agencies. Several states and Democrat party leaders have already challenged the president’s authority to appropriate funds this way.

In a surprise move, the Central Bank of Egypt cut its benchmark interest rates by 100bps on Thursday, thereby resuming the rate-cutting cycle which had been on pause since March 2018. The overnight deposit and lending rates now stand at 15.75% and 16.75% respectively, compared to y/y CPI inflation of 12.7% in January. The MPC communiqué justified its cut by reference to incoming data which ‘continued to confirm the moderation of underlying inflationary pressures.’

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Fixed Income

Treasury yields ended the week higher despite the release of weak economic data and strong rally in risk assets. The curve moved up with yields on the 2y UST, 5y UST and 10y UST closing at 2.51% (+5 bps w-o-w), 2.49% (+5 bps w-o-w) and 2.66% (+3 bps w-o-w).

Sovereign yields in the Euro area also closed higher in response to dovish comments from the ECB officials that alluded to possible TLTRO to address an economic slowdown that is stronger and broader than expected. Yields on 10y Bunds rose to 0.10%.

Regional bonds continue to trade in a tight range. The YTW on the Bloomberg Barclays GCC Credit and High Yield index has remained within 5 bps since the start of the month. It ended last week at 4.34% (-3 bps w-o-w). Credit spreads, however, tightened 8 bps w-o-w following a surge in oil prices.

Almarai was rated BBB- at S&P and Baa3 at Moody’s with a stable outlook. The company is looking to sell its first USD-denominated bond sometime this year.

FX

EURUSD posted a second week of losses, falling by 0.22% to close at 1.1296. This close is technically significant as it represents the second weekly close below the 200-week moving average (1.1335). As this level had provided support for the previous 15 weeks, its failure to halt losses is bearish for the price and while the cross trades below this level, further declines seem likely and a retest of the November 2018 lows of 1.1216 cannot be ruled out in the week ahead.

A 0.67% rise in USDJPY resulted a second week of gains and took the price to 110.47, close to our expectations last week for 110.50. Of technical significance is that the price was able to break above the formerly resistive 50-day moving average (110.18) on Tuesday and sustain closes above this key level for the remainder of the week. That the price has broken above this level for the first time in 2019 is technically bullish and the initial break of the 61.8% one-year Fibonacci retracement (110.73) was reversed, a retest of this level seems likely. Should this level be broken, it may result in a further climb towards 111.30, the 200-day moving average.

Following a 0.42% loss, GBPUSD fell for a third week to close at 1.2889. In the process, the fell below the 100-day (1.2877) and 50-day (1.2821) moving averages, falling as low as 1.2773 before recovering above these levels on Friday. However the price remained below the 23.6% one year Fibonacci retracement (1.2898) and the 14-week RSI (Relative Strength Indicator) is bearish in momentum which leads us to believe that further losses may lie ahead.

Equities

Regional equities started the week on a stronger footing. The DFM added +0.6% amid continued strength in Emaar-related named. Emaar Properties, Emaar Development and Emaar Malls added +2.0%, +3.5% and +1.9% respectively. du dropped -0.6% after the company reported full year net income of AED 1.75bn that missed consensus estimates of AED 1.86bn by 6%. Elsewhere, Aldar Properties rallied +3.6% to drive ADX index (+0.7%) higher.

Commodities

Both Brent and WTI futures extended their year-to-date gains last week and hit new high closes for the year. Brent added 6.7% last week to end at USD 66.25/b while WTI was up more than 5% to finish at USD 55.59/b. Risk assets generally performed well as markets expect an extension of the deadline on US-China trade talks, helping shore up sentiment amidst otherwise soft economic data.

Brent time spreads, relatively more influenced by OPEC issues than WTI, tightened last week into a more consistent backwardation in the first two years of the curve. Dec spreads for 19/20 closed last week at over USD 1.5/b, more than doubling their level at the start of the week. Long-dated WTI spreads have also been tightening but at the front end of the curve, the glut of US oil is still weighing on spreads: a contango is still in play for the first nine months of the curve.

Click here for the full document

Aditya Pugalia

Aditya Pugalia