Recent Search

Popular Searches

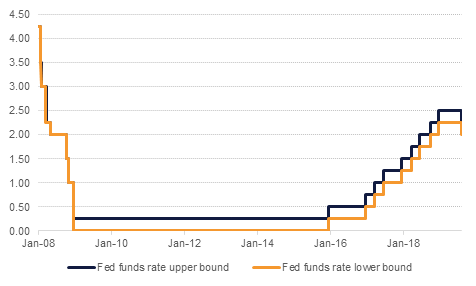

The U.S. FOMC cut interest rates by 25bps overnight as fully expected to a 2%- 2.25% range framing it as insurance against downside risks or weakness in global growth and trade, rather than the start of a longl easing cycle. In addition it was described as a “mid-cycle adjustment” which again was not a very dovish signal and argues against it being the start of many more cuts to come. For this reason the markets saw it as a relatively ‘hawkish’ cut with equities falling and the dollar strengthening in response, which actually had the effect of tightening financial conditions, precisely the opposite effect to the one intended. If this persists its will present a conundrum for the Fed and may renew the pressure for more cuts from the White House and from the markets. In particular given President Trump’s concerns about the strength of the USD it would not be a surprise to see him railing against the size of the Fed’s rate reduction quite quickly. The good news was that the Fed also decided to end its balance sheet adjustment a couple of months early, which was a more dovish signal. Meanwhile, there were two dissents with hawks Esther George and Eric Rosengren who voted for an unchanged rate stance.

Meanwhile economic growth slowed in the Eurozone in Q2 2019, with the economy expanding 1.1% y/y (0.2% q/q) compared with 1.2% y/y (0.4% q/q) the previous quarter. The slowdown in growth was broadbased and strengthens the case for the ECB to loosen monetary policy at the September meeting.

A downward adjustment to the Turkish Central Bank's CPI inflation projection for end-2019 from 14.6% y/y to 13.9% paves the way for further monetary easing in the country following the 425 basis point rate cut seen last week. Inflation slowed to just 15.7% in June, leaving the TCMB room to reduce rates, especially in the context of a more dovish turn by central banks globally. Newly installed governor, Murat Uysal, has said that a cautious stance will be maintained, but rate-cutting has support from President Recep Tayyip Erdogan and Finance Minister Berat Albayrak.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

The UST yield curve flattened somewhat as the US Federal Reserve cut interest rates by 25bps in a much anticipated move and halted balance sheet unwinding ahead of schedule. Yields on 2yr, 5yr, 10yr and 30yrs USTs closed at 1.87% (+2bps), 1.83% (-1bp), 2.01% (-5bps) and 2.52% (-6bps) respectively. Sovereign bonds across the pond also rallied in the face of weakening economic outlook. Yield on 10 yr Gilts declined 2bps to 0.61% and those on 10yr Bunds declined 4bps to -0.44% yesterday. Increasing possibility of supportive central bank policies kept the bid for risky assets intact, however credit protection costs reflected a mixed picture with CDS spread on US IG rising 3bps to 55bps while those on Euro Main declined a bp to 50bps.

Ahead of the Fed decision, regionally, GCC Bonds closed largely unchanged with average yield on Bloomberg Barclays GCC index remaining at 3.43% though credit spreads inched a bp higher to 149bps amid slight decline in oil prices. On the credit rating front, S&P yesterday affirmed QBE Insurance rating at A+ with a stable outlook.

In the primary market, Sharjah Islamic Bank has appointed banks to facilitate issuance of dollar denominated benchmark sized Tier1 sukuk.

The dollar rose in the aftermath of the FOMC. While the central bank cut interest rates, they did not indicate that it was the beginning of a cutting cycle (see macro). Since Wednesday morning, the Dollar Index (DXY) is trading 0.81% higher at 98.845, having reached a new 2019 high of 98.932 earlier this morning. The price is currently above the 76.4% five-year Fibonacci retracement (98.496) for the first time since May 2017. A daily close above this level may result in further gains for the dollar.

Global equities had a sell bias as trade talks between negotiators from the US and the China ended without much progress. Dow Jones and S&P 500 closed down by over 1% despite the interest rate cut in the US and FTSE 100 was down by 0.78%. Asia this morning has opened mixed with Hang Seng down 0.72% and Nikkei marginally up in early morning trades today.

Regional GCC markets were mixed amid marginally weakened oil prices. Dubai index was up by more than a percentage point, however, Abu Dhabi index closed lower mainly as a result of pressure on banking shares such as ADCB. Tadawul index was largely flat.

Oil markets ended the month roughly flat even as geopolitical tensions and trade war concerns pushed and pulled in opposing directions. Brent futures (the expiring September contract) closed up 0.7% overnight at USD 65.17/b while WTI added 0.9% to finish the month at USD 58.58/b. Average prices saw Brent up 1.9% m/m and WTI down by the same amount m/m.

The EIA reported a large draw in crude stocks of 8.5m bbl last week as well as declines in inventories across much of the rest of the barrel. The draw in stocks has been helpful in setting a floor under crude prices but we would note it is following a highly seasonal trend for the summer months of the year. US production ticked higher by 200k b/d to 12.2m b/d. Meanwhile, market surveys of OPEC production showed another decline in output to 29.42m b/d, the lowest collective level since 2011. Iran and Venezuela continued to report declining production as sanctions cut into both countries ability to export crude. Saudi Arabia also cut production, taking it to more than 300% compliant with its OPEC+ target. The scale of over-commitment to the production cut targets will raise risks of how much crude will be unleashed back onto markets when OPEC+ decides to end its production management.

A 25bps cut failed to give any succor to gold prices which dropped more than 1%, coming closed to breaking below USD 1,400/troy oz. As the Fed chair signaled that more rate cuts aren’t necessarily on the horizon and pointed to a still healthy performance in the economy, gold may find it difficult to push much higher without significant deterioration elsewhere in the global economy (eg, a breakdown in China-US trade talks).