Recent Search

Popular Searches

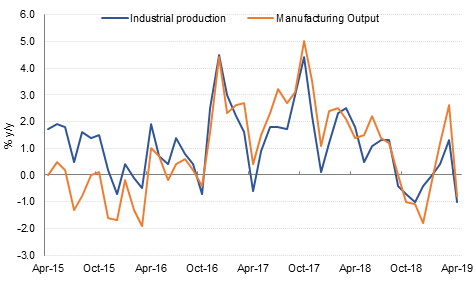

Sterling sold off yesterday on the back of much weaker than expected economic data in the UK. GDP declined -0.4% m/m in April, well below the consensus forecast of -0.1% m/m and also worse than the March reading. Both industrial production and manufacturing output contracted by more than expected in April, while construction output fell -0.4% m/m against a forecast for a 0.5% rise.

The contraction in April was likely due to the fact that many businesses had boosted inventory and brought forward production ahead of the end-March Brexit date, with output then falling in April. Some car manufacturers had also brought forward their annual shutdowns from August to April because of the initial Brexit deadline, and that would have contributed to the drop in factory output last month. Meanwhile, a record 10 conservative MPs have been formally nominated to replace Theresa May as leader of the party and prime minister, including Boris Johnson, Michael Gove and Jeremy Hunt. Conservative MPs will shortlist two candidates before party members vote by post next week. Results are expected the week of 22 July.

US job openings remained near record highs in April at 7.45 million, according to the JOLTS data released yesterday. The “quits rate” remained at a near 15-year high of 2.3%, suggesting that workers were still very confident about their ability to find new work in April. However the recent disappointing non-farm payrolls data suggests the job market was softer in May.

CPI inflation in Egypt ticked up to 14.1% y/y in May, from 13.0% in April, driven by food and drink. Upcoming subsidy reforms to energy and fuel expected at the start of the next fiscal year (starting July 1) will likely maintain pressure on prices, even as base effects from last year’s tariff hikes will offer some mitigation as they pass through. Having held rates steady at its May MPC meeting, the CBE is unlikely to cut over the next several months given this inflationary environment.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Treasuries gave up a part of their last week gains as investors’ possibly locked in some gains and as tariffs on Mexico were averted. Yields on the 2y UST, 5y UST and 10y UST closed at 1.90% (+6 bps), 1.91% (+6 bps) and 2.14% (+6 bps) respectively.

Regional bonds traded flat as most investors in the GCC returned from the week-long holiday. The YTW on Bloomberg Barclays GCC Credit and High Yield index was unchanged at 3.73%. However, credit spreads tightened 5 bps to 169 bps.

In terms of rating action, Fitch affirmed Emirates Islamic Bank and Abu Dhabi Islamic Bank at A+ with stable outlook.

The USD index strengthened modestly yesterday, following the weakness after Friday’s disappointing payrolls data.

However the main move among the currency majors yesterday was sterling, which fell around -0.7%. Softer than expected GDP, industrial output and construction output data contributed to the decline and the conservative party leadership election kicked off in earnest yesterday as well, and this is likely to keep the pound under pressure in the near term.

Developed market equities closed higher as investors’ remained positive on easing in monetary policy. The S&P 500 index and the Euro Stoxx 600 index added +0.5% and +0.2% respectively.

Regional equities rallied as they continued to catch up with moves in global markets last week. The DFM index and the Tadawul gained +0.9% and +1.7% respectively. Dubai Islamic Bank gained +1.6% after the bank’s board recommended buying Noor Bank.

Oil markets started the week on a softer footing after warnings from Russia’s finance minister that oil prices could dip back to USD 30/b if there is no deal by OPEC+ countries on maintaining production cuts and further anxiety over US tariffs following US president Donald Trump again threatening tariffs on Mexico. Brent futures closed down 1.58% at USD 62.29/b while WTI fell to USD 53.26/b, down 1.35%.

Russia’s deputy energy minister said that OPEC+ would reach a “consolidated” decision by the end of June on whether to extend current oil production cuts. Russian oil companies are divided on whether to maintain or end the cuts and Russian president Vladimir Putin has said that there is division between OPEC and Russia over what a fair price for oil should be.