Recent Search

Popular Searches

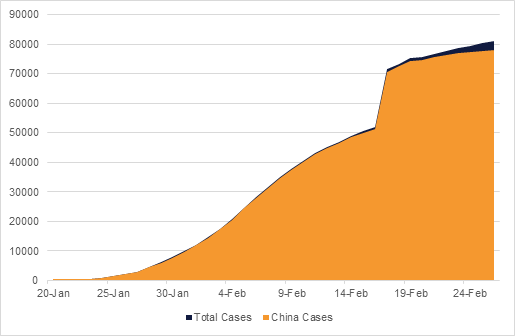

The Coronavirus outbreak remains to the fore in headlines and market moves, with new cases reported in a host of countries in recent days. In Europe there have been new cases in Austria and Greece, Latin America has seen its first case in Brazil, and regionally Pakistan has now reported two cases. Travel bans and restrictions have been ramped up globally, and Saudi Arabia has announced a temporary ban on Umrah pilgrims. There have been statements from global leaders, with US Vice President Mike Pence put in charge of the country’s response and the Chinese Politburo cautioning that the outbreak could dent its anticipated acceleration in growth.

The chance of a v-shaped recovery is becoming ever more distant as the disease metastasizes, and some sort of monetary and fiscal response from authorities is becoming more likely. The market-implied probability of a rate cut by the US Fed this year has risen from one in January to two now fully priced in, and the PBOC has said that it is considering cutting the benchmark deposit rate for the first time in five years. Christine Lagarde of the ECB is due to speak later today. In terms of fiscal response, Hong Kong announced a windfall of HKD 10,000 for permanent residents, and the interim Malaysian Prime Minister Mahathir is scheduled to announce a stimulus package today.

In the US, new home sales hit 764,000 in January, m/m growth of 7.9% and far stronger than expectations of 718,000. The sector is benefitting from low interest rates, and could continue to do so as the coronavirus pushes longer-dated treasuries lower.

Source: WHO situation reports, Emirates NBD Research

Source: WHO situation reports, Emirates NBD Research

Treasuries extended their rally as more governments issued warnings regarding coronavirus. None of them expressed confidence that they are on top of the situation which in turn fueled risk-off mood. Yields on the 2y UST and 10y UST closed at 1.16% (-6 bps) and 1.33% (-2 bps) respectively.

The continued worries over economic impact of coronavirus has forced regional investors to lock in their gains.. The YTW on Bloomberg Barclays GCC Credit and High Yield index rose +4 bps to 2.90% while credit spreads widened 6 bps to 162 bps.

The dollar index has dipped to 98.6, weakening against the bulk of its peers after a case of coronavirus was reported in the US with an unknown origin. The move towards an expectation by the market of two rate cuts this year is likely also playing a part in recent relative dollar weakness. As a result, the AUD, which has been trading at 11-year lows, saw some respite, picking up 0.2% to 0.6557 this morning.

Regionally, the Egyptian pound has weakend from its multi-year highs at the start of the week, losing 0.2% over the past two days. This is in line with EM FX generally, as risk aversion has put pressure on riskier currencies. The JP Morgan EM FX index has fallen to 58.634, a new low for the 10-year series.

Developed market equities closed mixed as attempts to rebound from days of weakness failed. The developments regarding coronavirus remains severe. The S&P 500 index dropped -0.4% while the Euro Stoxx 600 index closed flat.

Regional equity markets closed lower as global cues remained weak. The sell-off was broad based with the DFM index and the Qatar Exchange dropping -2.0% and -1.6% respectively. Air Arabia (-2.1%) dropped for a fifth consecutive trading session to close at the lowest level since November 2019.

Both brent and WTI futures have resumed their slide, closing down 2.3% and 2.8% respectively yesterday, and have continued to weaken today, to levels last seen in December 2018. WTI is trading at USD 48.1/b, while brent has dipped to USD 52.8/b.

Demand fears around the coronavirus impact are to the fore, and there has as yet been no clear indication from OPEC+ as to the implementation of proposed cuts. Even a much smaller than anticipated expansion in US crude stocks – 452,000 bbl, compared to an expected 2.6mn bbl – did little to slow the decline in prices.

Daniel Richards

Daniel Richards