Recent Search

Popular Searches

Chinese markets opened sharply weaker this morning, in the first day of trading since the Chinese New Year holidays. Equities declined around -8% as did most commodities, while the yuan weakened above 7/USD and bond yields declined the most since 2014. The PBOC injected a net 150bn yuan of liquidity into the system this morning through reverse repos, at lower rates. The PBOC had announced over the weekend that it would take steps to ensure liquidity and stability in the financial system, including extending grace periods to meet regulatory requirements and easier access to financing for affected companies. The risks to global economic growth posed by the novel coronavirus continue to escalate, as the WHO declared a global health emergency at the end of last week, and Apple joined other multinationals in announcing the closure of its stores across China until 9 February. Growth estimates for China have been revised lower by several financial institutions, but the risks to global growth also come from disruptions to supply chains, with factories remaining shut and many flights cancelled.

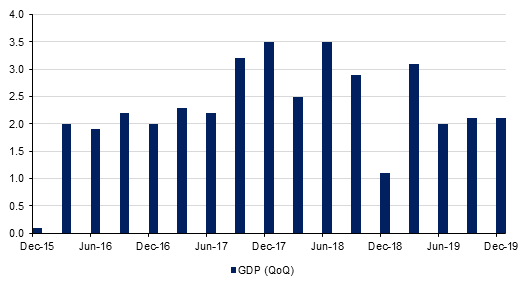

The US economy grew 2.1% in Q4 2019, the same rate as Q3 and slightly better than the consensus forecast of 2.0%. However for 2019 as a whole, GDP growth slowed to 2.3% from 2.9% in 2018, the slowest growth rate since 2016. Moreover, consumer spending – which has been the main engine of growth in prior quarters – slowed to 1.8% in Q4 from 3.2% in Q3 2019, and was below expectations. Business investment was also weak. On the positive side, home building grew at the strongest pace in two years, and net exports was a key contributor to overall GDP growth in Q4. Eurozone GDP growth was weaker than expected in Q4 2019, expanding just 0.1% q/q and 1.0% y/y. France and Italy both recorded a contraction in Q4, with some of the weakness in France due to strikes. The data supports our view that the ECB is likely to ease monetary policy further this year through QE.

In an attempt to revive economic growth in India, the FY 2021 budget included a combination of increased capital expenditure plans and an optional rationalization in income tax rates. Further measures to attract foreign investments were also announced including tax breaks for sovereign wealth funds and enhanced limits for investment into bonds. Unsurprisingly, the measures announced forced the government to use the escape clause in the FRBM act as it breached deficit targets. The fiscal deficit for FY 2020 is now estimated at 3.8% (versus 3.3%) and at 3.5% for FY 2021.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Treasuries closed higher as the Federal Reserve delivered a rather dovish view even as it kept rates on hold at its last week meeting. The sustained risk-off mood on account of continued fears over the coronavirus also helped USTs. The curve steepened with yields on the 2y UST and 10y UST ending the week at 1.31% (-18 bps w-o-w) and 1.50% (-17 bps w-o-w). Yields on 30y USTs closed below 2% for the first time since August 2019.

Notwithstanding a sharp sell-off in emerging markets assets and oil prices, regional bonds moved higher. The YTW on Bloomberg Barclays GCC Credit and High Yield index dropped -10 bps w-o-w to 3.0% and credit spreads widened marginally to 153 bps (+5 bps w-o-w).

A 0.64% increase in the price was able to help EURUSD void the declines of the previous week and close at 1.1093 on Friday. The move was mainly driven by gains on Friday following initial declines earlier in the week. Technical analysis of the daily candle chart shows a few noteworthy observations. Firstly, the break below the 23.6% one-year Fibonacci retracement (1.1018) was not sustained. In addition to this, the price has broken back above the 100-day moving average (1.1071). Over the next week, a daily close above the 50-day moving average (1.1099) and the 38.2% one-year Fibonacci retracement (1.1103) would likely result in a larger move towards the 1.12 level.

A 1.01% rise took the price of GBPUSD back above the 1.32 level with the price finishing the week at 1.3206. This increase was accompanied by two key developments. Firstly, there was a break above and two consecutive closes above the 50-day moving average (1.3073). In addition the 76.4% Fibonacci retracement (1.3147) which had provided resistance for the previous two weeks was firmly pierced. This is a bullish development for GBPUSD and while the price remains above this level, we expect further gains for GBPUSD.

Regional equities closed lower following weak global cues over the weekend. The DFM index and the KWSE PM index dropped -0.9% and -0.5% respectively. The weakness was rather broad based with all sectors bearing the brunt of sell-off.

Oil markets continued to crumble as uncertainty over the oil demand impact of the coronavirus outbreak gives way to anxiety that China’s oil consumption growth, among others, will be severely curtailed. Brent futures for March expiry settled at USD 58.16/b, a weekly drop of 4.2% and taking Brent down nearly 12% year to date. WTI futures settled down at USD 51.56/b, a loss of 4.9% week on week and a decline of almost 16% year to date. The risk of oil futures starting the year in a bear market looks particularly acute as a move away from risk assets generally drags commodities downward.

Market structures slumped in line with the drop in front month prices. The WTI curve is now in contango for the first three months while the backwardation in Brent is continuing to shrink. December spreads have displayed a substantial weakening with Dec 20/21 spreads closing in a backwardation of just USD 0.7/b in Brent (compared with USD 4/b in early January) while in WTI the same spread closed last week at just above USD 1/b. Risk reversal structures (25 delta) for April Brent futures have still not priced in much downside risk with puts trading at a relatively muted premium to calls.

Aditya Pugalia

Aditya Pugalia