Recent Search

Popular Searches

Labour data from the UK showed workers earning higher wages in the three months to August while overall unemployment held steady at 4.3%. Wage growth expanded 2.2%, slightly faster than market expectations while unemployment is holding near its lowest levels in more than 40 years. The labour figures come a day after UK CPI showed a jump up to 3%, highlighting how workers are grinding against higher prices even as the labour picture looks sanguine. For the Bank of England the positive labour data and elevated inflation make balancing an expected rate hike challenging with overall economic output that has been drifting.

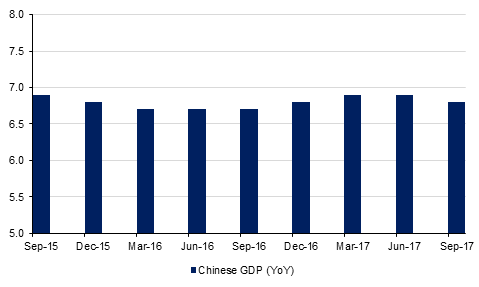

China’s economy slowed in Q3, expanding by 6.8% y/y compared with 6.9% in Q2. The decline in GDP growth was in line with market expectations as the authorities in China had been taking steps to try and control rampant property activity and get to grips with a large debt overhang, particularly at the province-level. Overall the GDP performance falls neatly in line with China’s targeted growth of 6.5% this year, leaving room for a further slowdown in Q4. Also in China factory output in September expanded by 6.6% y/y, better than the market had expected and faster than August while fixed asset investment slowed further to growth of 7.5%.

The Federal Reserve’s Beige Book gave an upbeat assessment of US economic performance in September-October despite several regions being affected by hurricane damage. In its Beige Book, the Fed noted that despite a tightening labour market most Fed districts only reported ‘modest to moderate’ wage pressures. US president Donald Trumps is set to make his pick for the next chair of the Fed in ‘coming days’, according to press reports with the race seemingly still competitive between all potential candidates. Mr Trump meets Janet Yellen, the incumbent chair, later today with the market likely to parse their interactions closely given the president’s tendency to favour officials with whom he can build rapport.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

The guessing game over who will be the next Fed chair kept bond investors on the edge, pushing treasury yields up across the curve. Traders are hedging against the risk that John Taylor, who is perceived as the most hawkish of the five candidates on the President’s short list, may end-up as Trump’s pick. Yield on 2yr, 5yr, 10yr and 30yr UST closed at 1.56% (+2bps), 1.99% (+3bps), 2.35% (+5bps) and 2.85% (+5bps) respectively. Yields on sovereign bonds across the Atlantic also increased in sympathy with 10yr Gilt yields rising to 1.31% (+4bps) and Bunds to 0.39% (+3bps). Credit spreads were range bound with CDS levels on US IG and Euro main closing unchanged at 54bps and 55bps respectively.

Regionally, credit spreads had a mixed performance. CDS levels on Dubai and KSA tightened to 123bps (-2bps) and 83bps (-1bp) respectively while those on Qatar widened by a bp to 102bps. Cash bonds also reflected mixed performance. Average yield rose in sync with the benchmark yield albeit somewhat balanced off by credit spread tightening. Barclays GCC index closed with YTW at 3.42% (+1bp) and option adjusted spread at 131bps (-2bps).

Activity is the primary market is robust with Apicorp on the road for a benchmark sized dollar denominated sukuk and Bahrain’s Oil and Gas Holding Company (NOGA) providing initial guidance of high 7% for its 10yr USD benchmark offering.

In a market with risk appetite, JPY underperformed on Wednesday, softening against the other major currencies. Over the course of the day USDJPY rose for a third consecutive day, gaining 0.66% to close at 112.94 and reinforce the break out of the former daily downtrend that had been in effect. While the cross stays above the 200 day MA (111.76) and 61.8% one year Fibonacci retracement, we expect further gains towards 114.50 in the medium term. The risk of this outcome is compounded further by the pattern of Q4 seasonality in USDJPY price action to be biased to the upside.

As we go to print GBPUSD trades at 1.3213, trading 0.54% lower than at the start of the week. This afternoon, markets will be awaiting retail sales data which are expect to show a 0.2% m/m contraction in September. Should the data show a bigger decline than this, it can be expected that we shall see a larger decline in cable.

Equity benchmarks advanced in most of the developed world though were flat in Asia despite China reporting healthy GDP growth of 6.8% in Q3. The S&P 500 index hit another all-time high overnight, boosted by solid earnings announcements. In contrast Hong Kong’s Hang Seng Index was down 0.1% and the Shanghai Composite Index slid 0.8%.

Regional equities had mixed performance. Dubai (+0.06%) and Abu Dhabi (+0.30%) gained mostly due to improvement in banks and property companies’ shares while Tadawul (-0.28%) fell. Qatar’s index lead the losses closing down by -1.03%.

Oil markets perked up slightly yesterday as a draw in US inventories and a decline in production reported by the EIA helped boost prices. Brent futures closed up 0.47% while WTI ended the day higher up 0.3%. Production in the US was affected by Hurricane Nate and output fell more than 1m b/d but judging by past responses to hurricanes, we would expect the recovery to be reasonably swift.

Market chatter is suggesting OPEC will agree to a nine-month extension of its existing production cuts with its partners, taking the cuts to the end of 2018 instead of just the end of Q1. If OPEC succeeds in extending and enforcing the cut then the oil market balance would appear much healthier next year but the pressure to stick with the deal and limit production may be severely challenging for OPEC economies to endure.