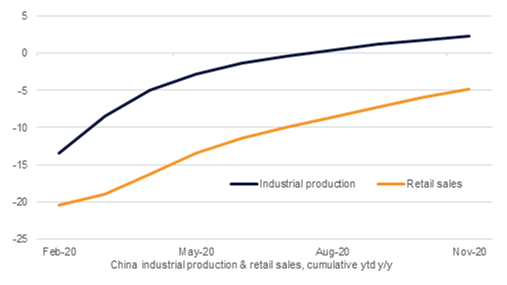

- There were a series of robust data releases from China this morning, giving strength to expectations of a durable recovery from the pandemic crisis next year. The recovery is now being driven by both production and consumption, with retail sales up 5.0% y/y in November (accelerating from 4.3% in October) and industrial production up 7.0% (up modestly from October’s 6.9%). The production side remains the stronger over the year to date, however, up 2.3% now, while retail sales remain down -4.8%.

- In the Eurozone, industrial production expanded 2.1% m/m in October, narrowly beating expectations of 2.0% growth. This reading preceded the most recent wave of Covid-19 infections and related restrictions on activity, however.

- The pandemic continues to pose a threat to European growth. Following on from the restrictions imposed in Germany in recent days, much of England’s southeast, including London, was placed under stricter limits yesterday. The Bank of England is set to meet this week, but barring any decisive moves one way or another on Brexit, the bank will likely look to conserve its firepower for now.

- Dubai’s PMI survey slipped to 49.0 in November, down from 49.9 the previous month. Business optimism was particularly weak, slipping into negative territory for the first time as concerns regarding the pandemic remained to the fore. Job shedding slowed to its weakest pace in months, however.

Recovery in progress in China

Source: Bloomberg, Emirates NBD Research

Fixed Income

- Treasuries ended the day relatively unchanged despite some wide intraday moves. After sinking in the early session a pronounced risk-off tone took hold once the US began trading with equities sinking there and USTs rallying at the end of the day. The gain are continuing—modestly—this morning with yields on the 10yr UST down below 0.9% at 0.8898%.

- Bonds were broadly higher across geographies and asset classes with both high yield and emerging market bonds gaining. Regionally, the primary market is quiet.

FX

- The US dollar experienced some choppy trading overnight but ultimately ended the day down by 0.3% on the DXY index. In early trading today the greenback is continuing to slip as concerns that new virus-related restrictions may need to be imposed in the US.

- Sterling was the main winner at the start of the trading week as an extension to talks between the UK and EU raised hopes that a Brexit deal could be in the offing. GBP rallied 0.8% to close the day at 1.3324 and is extending gains in early trade today. The Euro managed a gain of 0.26%, rising to 1.2144.

Equities

- Equities largely started the week on a moderately positive footing, although some of the animal spirits seen earlier in the session later faded, especially in the UK as the FTSE 100 ultimately closed down 0.2%.

- Elsewhere in Europe, the CAC and the DAX both closed higher, gaining 0.4% and 0.8% respectively, despite the new restrictions in Germany.

- Within the region, the DFM gained 0.3% and the Tadawul 0.2%, while in the US, the NASDAQ closed 0.5% higher, but the Dow Jones (-0.6%) and the S&P 500 (-0.4%) both ended the day lower.

Commodities

- Oil prices were higher overnight, supported by a geopolitical risk element thanks to an explosion near a port in Saudi Arabia. Brent futures rallied 0.6% to close above USD 50/b while WTI was up nearly 1% to settle just short of USD 47/b.

- OPEC revised its outlook for 2021 oil demand growth lower in its latest monthly oil market report as the producers’ bloc assessed the “uncertainty” around the effects of Covid-19 on oil demand. Broadly the outlook is for robust growth of 5.9m b/d although much of that will be at the back end of the year.

Click here to Download Full article

Daniel Richards

Daniel Richards