Recent Search

Popular Searches

China’s rebound from its Covid-induced slump has been muted even if the data is still trending higher. Industrial production was up 2.4% y/y in the first two months of 2023, its slowest pace of expansion since 2020 and slightly slower than market expectations. Fixed-asset investment was more positive, up by 5.5% in the first two months of the year and ahead of both the previous reading and market expectations.

China’s manufacturing sector is recovering with the latest official PMI hitting 52.6 for February, its strongest reading since 2012, while the non-manufacturing PMI, which includes construction activity, jumped to 56.3 in February compared with prints as low as 41.6 as recently as December last year. The construction sub-component was particularly robust, hitting 60.2 in February, up from 56.4 a month earlier.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

But so far, the data doesn’t seem to have put a fire under commodity markets as the approach from China’s economic leadership seems to be for steadier, more manageable growth rather than trying to foster a boom-bubble cycle that could potentially worsen the country’s property market travails. Real estate investment was still negative in the first two months of the year, down by 5.7% y/y though an improvement from the 10% drop recorded at the end of 2022. The country’s growth target of 5% for 2023 is a shade of historic performance and may also be serving to dampen enthusiasm that China will have a voracious appetite for industrial commodities this year.

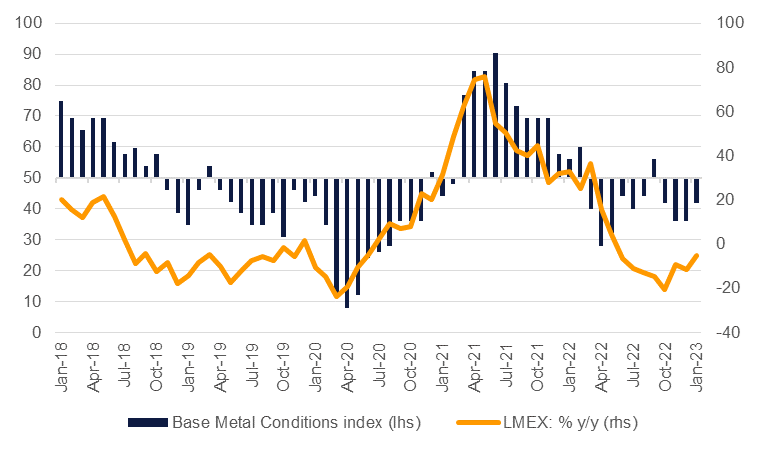

Prices for major industrial metals have had a relatively muted start to the year. After an initial pop higher in the first few weeks related to the optimism around China’s reopening, prices for aluminium, copper and iron ore have held to relatively narrow ranges. The LMEX index of six base metals has slipped 1% since the start of the year as a 5.5% gain in copper forwards has been balanced by declines across the rest of the complex: aluminium is down by a meagre 1% but nickel prices have fallen by 23% since the start of the year.

The narrative around China’s recovery this year, and its potential to lift other emerging markets, is positive but is being strongly counterbalanced by market anxiety that the rapid pace of monetary tightening—whether from the Federal Reserve in the US or the European Central Bank—will over-tighten financial conditions and prompt a recession in major economies.

A persistently strong dollar also doesn’t help commodity prices in the near term, even if the dollar’s strength looks as though it is beginning to ebb. Financial stability concerns will be another near-term headwind for industrial metals as investors flock to haven assets though the actions taken by monetary authorities and financial regulators appears to be helping stave off contagion worries.

We remain constructive on the outlook for industrial metals given that China’s rebound has room to run and is likely to be buttressed by more supportive policies, particularly toward the property market. The potential of an earlier than anticipated end to the US rate hiking cycle, at least as priced in by markets, should also boost demand for risk assets like commodities.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Edward Bell

Edward Bell