Recent Search

Popular Searches

China’s real GDP growth slowed to 6.5% in Q3 according to data released at the close of last week, lower than both expectations of 6.6% and Q2 growth of 6.7%. Indeed, this was the slowest pace of growth since the midst of the global financial crisis in 2009. The slowdown was driven by weaker domestic demand, while exports held up. However, with trade war threats still looming the Chinese government is dialling back on some of its deleveraging efforts in a bid to support growth, and the reserve requirement was already cut earlier in October. There was also support pledged for the stock market last week, as the China Securities Regulatory Commission unveiled measures including speedier approval for mergers and acquisitions and support for SMEs to issue high-yield bonds.

Italy’s government spending plans continue to cause concern, having raised the consternation of both the European Commission and Moody’s at the close of last week. The ratings agency cut Italy’s sovereign debt rating to just one notch above junk status, while the EC declared that the proposed budget was an unprecedented deviation from targets with serious non-compliance. The EC have asked Italy for clarity on its real GDP growth projections, which it finds overly bullish, and for an explanation as to why it is loosening fiscal policy when it had previously pledged to draw down the deficit. The spending plan currently envisages a shortfall equivalent to 2.4% of GDP.

The minutes of the last Reserve Bank of India’s monetary policy committee (MPC) meeting were released over the weekend. The minutes reaffirmed the view that the MPC remains on a wait and watch mode and that the focus of the members remains on inflation data. The minutes also confirmed that the change in stance to ‘calibrated tightening’ means there will be no rate cuts in the current cycle even if the central bank is not obliged to raise rates at every meeting. Overall, the minutes and inflation data following the meeting indicates that the policy rates may remain on hold longer than earlier anticipated.

Treasuries closed lower. However the pace of change slowed as geopolitical developments weighed on risk assets. Yields on the 2y UST, 5y UST and 10y UST closed at 2.90% (+5 bps w-o-w), 3.04% (+3 bps w-o-w) and 3.19% (+3 bps w-o-w) respectively.

Italian bonds rallied on positive developments. The yield on the 10y Italian government bonds dropped 10 bps to 3.47%. Even as Moody’s cut Italy’s rating to Baa3, the outlook was kept at stable which in turn helped reduce the risk of junk ratings in the immediate future.

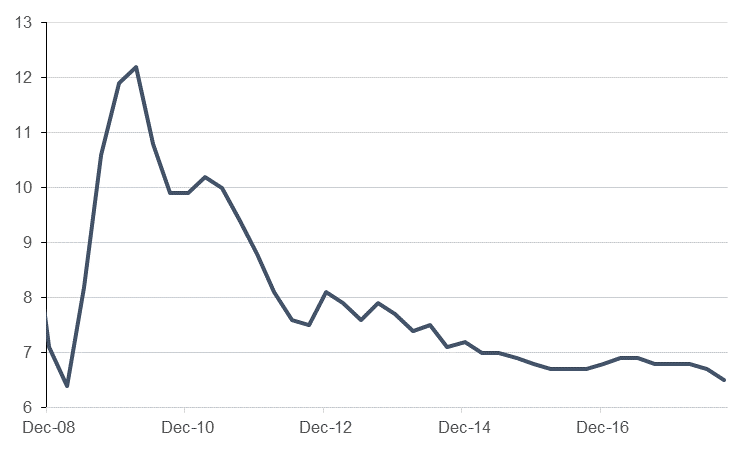

Regional bonds continued to drift lower for a third consecutive week. The decline tracked moves in broader markets. The YTW on the Bloomberg Barclays GCC Credit and High Yield index rose +6 bps w-o-w to 4.65% and credit spreads remained flat at 165 bps.

Fitch assigned Tabreed a rating of BBB with a stable outlook. The agency attributed the rating to low-risk business profile with traditional utility-like features.

Over the last week, the dollar gained 0.47%, the Dollar Index rising to 95.666. Over the course of the week, the index found support at the 100-day moving average (94.92) and was able to break and secure three consecutive closes above the 50-day moving average (95.224). During the week ahead the markets will be eying economic data from the US including advance Q3 2018 GDP data and PMIs. Any downside surprises in the data may prompt a retest of the 100-day moving average. A daily close below this level (and the 76.4% one-year Fibonacci retracement) puts the index at risk of further declines towards the 92.60 level.

Regional equities started the week on a negative note. Most indices closed lower with the DFM index and the Qatar Exchange losing -0.8% and -0.4% respectively.

After the market closed, ADCB reported Q3 2018 and 9M 2018 net profit of AED 1.15bn (+5.5% y/y) and AED 3.48bn (+9.0% y/y). Net loans for the bank grew +1.0% since December 2017 while deposits increased +4.0% over the same period.

Oil benchmarks weakened a second week running as concerns over supply constraints gave way to emerging anxiety about crude demand in 2019. Brent prices fell 0.8% over the course of the week to close at USD 79.78/b while WTI lost more than 3% to close back below USD 70/b. Strong Chinese refinery demand in September (12.49m b/d) was an outlier in otherwise weak economic growth in Q3: GDP rose 6.5% y/y compared with 6.7% in the previous three months. The full impact of the US-China trade war will hit markets in 2019 and could act as a considerable drag on oil demand next year, raising the possibility of the market returning to surplus.

The WTI market already appears to be pricing in that outcome as the forward curve closed in contango for the first five months. The flip of the curve is a significant turnaround from the backwardation over as much as USD 2.5/b on the 1-2 month spread that WTI saw this summer. The move into contango reflects the persistent upward climb in US production, despite a shortage of takeaway pipeline capacity, and a steady increase in US crude stocks. So far the move in the US benchmark hasn’t brought down the Brent curve in sympathy and the uncertainty over whether other OPEC members can replace the drop in Iranian volumes will likely keep Brent better supported until demand weakness becomes more apparent. Indeed, Brent-WTI closed again back below USD 10/b at the end of the week.

Gold prices added nearly 0.7% last week for their third consecutive weekly gain, the longest stretch since the start of the year. Prices ended the week at USD 1,226/troy oz.

Daniel Richards

Daniel Richards