Recent Search

Popular Searches

There was no new announcement on the US – China trade talks though substantive progress is believed to have been made and discussions seemed to have moved from trade wars to trade peace. In the interim, China lowered its official goal for economic growth in 2019 to a range of 6% to 6.5% as exports as well as domestic demand shows signs of deceleration. It also announced a cut of 3% in VAT payable by the top bracket in a move aimed at benefiting the manufacturing sector.

The Reserve Bank of Australia left policy rate unchanged at 1.5% for the 28th consecutive meeting, citing slow progress on inflation which remains below the bank’s target despite unemployment rate at only 5%.

Regional PMI data for February was somewhat disappointing, with the UAE’s headline index falling to the lowest level since October 2016 and Egypt’s PMI remaining in contraction territory. Only Saudi Arabia’s PMI was slightly firmer than in January, underpinned by strong domestic demand. The common theme across all three surveys was weak private sector employment. The UAE’s employment index fell to a record low, while employment in Egypt was a shade under the neutral 50-level last month. Even in Saudi Arabia, where both new orders and output rose at a faster rate than in January, employment was broadly unchanged last month.

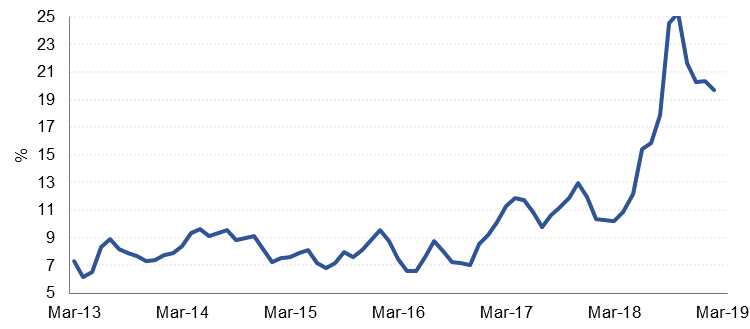

In Turkey consumer prices in February rose 19.7% y/y, slower than the 20.4% recorded in the previous month and below the consensus of 19.9%. Inflation is getting tamed as the lira has stabilized somewhat and various short-term measures implemented by the government to rein in inflation, particularly in terms of food prices, have started to take effect. While food inflation decelerated to an annual 29% from 31% in January, it’s still running well above the central bank’s year-end forecast of 13%. The central bank may wait for sustained deceleration of inflation before resuming monetary easing and is expected to leave interest rates unchanged at 24% at its meeting on Wednesday. Also Turkey’s trade deficit in February narrowed to USD 1.85bn after exports rose 4% to USD 14bn and imports fell 19% to USD 16bn.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Risk appetite faded a little as there was no new concrete announcement on trade talks, causing safe haven assets like the UST treasuries to rise. Yields on 2yr, 5yr, 10yr and 30yr USTs closed lower at 2.54% (-1bp), 2.53% (-3bps), 2.72% (-3bps) and 3.09% (-3bps) respectively. Sovereign bonds across the Euro area were also in demand with yields on 10yr Bunds and Gilts falling to 0.16% (-3bps) and 1.27% (-2bps) respectively.

Regionally, notwithstanding the falling benchmark yields, average yield on Barclays GCC bond index increased 2bps to 4.29% as credit spreads widened by 4bps to 169bps on the back of receding appetite for risk assets.

Monday’s gains have taken the Dollar Index to near two-week highs as the USD continues to remain supported by treasury yields. A large part of the index’s performance may be attributed to softness in the EUR ahead of Thursday’s ECB meeting. While data in the Eurozone has showed slowing growth, U.S. economic data has remained resilient and investors may be expecting a dovish tone from the ECB on Thursday to contrast with the Federal Reserve's upbeat view of the U.S. economy. As we go to print, the DXY is trading at 96.627.

Elsewhere AUDUSD endured less volatility than expected in the aftermath of the RBA meeting at which policy makers kept interest rates at a record low of 1.50%. With the central bank shifting from a tightening to neutral bias last month, had policy makers been more dovish, AUDUSD could have plummeted below the 0.70 handle. Presently AUDUSD is trading at 0.7077.

Developed market equities were mixed overnight. The S&P 500 gave up 0.39% while the FTSE gained the same amount while the Dax was essentially flat. Profit taking, on signs of a pending US-China trade deal, was a likely catalyst behind the negative move in US equities along with disappointing construction data for December, potentially heralding a downward revision to Q4 GDP estimates.

The Tadawul was the main gainer among regional equity markets, up 0.4% overnight while the DFM was little changed and the ADX fell 0.4%.

Oil markets have started on a softer footing today as official downgrades to China’s growth expectations will weigh on sentiment for demand. Brent futures are currently trading around USD 65.40/b while WTI is at USD 56.32/b. OPEC appears to be delaying a decision on whether to extend its current production cuts until June, rather than the regularly scheduled April meeting. We expect official output cut targets to be maintained but increasingly ignored over the year as unplanned production outages in countries like Iran, Venezuela or Libya allow for other producers to creep production back into markets.

Industrial metals so far haven’t shown much reaction to the lower China GDP growth forecast. The government will be providing stimulus in the form of lower taxes (including in manufacturing and construction). While less immediately impactful on growth, the indirect stimulus should still help to keep demand for capital inputs steady, if not spectacular.