Recent Search

Popular Searches

.jpg?h=457&w=800&la=en&hash=500BA47759B20E04C1D8829761CC8153)

China cancelled talks that were scheduled for this week and warned President Trump that his threats of further tariffs are blocking any potential negotiations. President Trump threatened to impose higher tariffs on the remaining Chinese imports should Beijing retaliate against Monday’s round. As China has said that step is certain, the stage appears set for yet another escalation of the trade war. On the other hand, President Trump signed his first free trade agreement with South Korea yesterday. This is the first major trade deal the president has finalized since entering office. Although South Korea is only the 6th largest trading partner of the US, it is the second largest importer of beef.

President Trump will address the full UN General Assembly and then host a UN Security Council session today where the discussion agenda include Iran and North Korea. Coming days could bring few politically charged news articles as the world leaders meet in New York to broadly address issues relating to proliferation of weapons of mass destruction. On the economic front, Chicago Fed National Activity Index came in at 0.18 vs expectations of 0.20 while July was revised up to 0.18 from 0.13. The index points to steady economic growth in August.

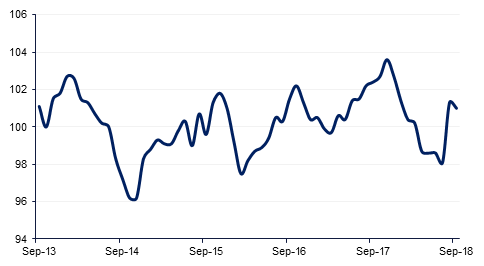

The lack of progress in Brexit talks appears to be causing a drag on investments in the UK and forcing some companies to start rolling out their plans for a no-deal outcome. U.K. manufacturing growth appeared to have cooled to a four-month low in September as foreign demand softened. The Confederation of British Industry’s gauge of total orders slipped to minus one this month, from seven previously. Across the English Channel, the September reading of the German IFO survey reflected slight decline from 103.9 to 103.7 though still better than the consensus. On recent form, the IFO still looks consistent with very healthy annual GDP growth of over 2% this year.

ECB President, Mario Draghi, yesterday at a conference, said that inflation in the Eurozone will be ‘relatively vigorous’. Although his statement was not backed by any fresh data or projections, market took it as a sign of more hawkish ECB going forward.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

Treasuries were marginally lower across the curve following a sell-off in bunds. Activity in US markets remained subdued. Yields on the 2y UST, 5y UST and 10y UST closed at 2.81% (+2 bps), 2.96% (+2 bps) and 3.08% (+2 bps) respectively.

Regional bonds continued to trade in a tight range. The YTW on the Bloomberg Barclays GCC Credit and High Yield index remained flat at 4.50% while credit spreads tightened 1 bp to 160 bps.

Aldar Investment raised USD 500mn in a 7-year sukuk which was priced at 170 bps over midswap. Elsewhere, Moody’s assigned A1 ratings to proposed offering from Sabic.

The GBP outperformed on Monday, gaining on all the major currencies after being given a boost by the news that Comcast was coming close to an acquisition of sky and the news that the Labour Party may press for a second Brexit referendum. Over the course of the day GBPUSD rose 0.37% to reach 1.3120, but from the GBP crosses, EURGBP which also fell 0.37% to reach 0.89541 is more noteworthy. While the price found support close to the 50-day moving average (0.89449), and the supporting baseline of the weekly uptrend that has been in effect since the 24 June 2016 (the day of the Brexit referendum), it remains below the 76.4% one-year Fibonacci retracement (0.89859). While the daily closes remain below this level, there is further downside risk for EURGBP.

Developed markets closed mainly in the red on Monday with the Dow Jones falling 0.68% while the S&P500 fell by 0.35% and the Nasdaq rose by a modest 0.08%. In Europe, the outcome was equally gloomy and the Euro Stoxx fell 0.59%, DAX declined by 0.64% and the FTSE closed 0.42% lower.

Regional markets suffered minor losses with the ADX and DFM retreating 0.10% and 0.30% respectively.

As we go to print, Asian markets have opened with mixed results and while the Nikkei is currently up by 0.12%, the Shanghai composite is currently 0.76% in the red.

Brent futures settled above USD 80/b for the first time since 2014, closing up more than 3% at USD 81.20/b. WTI followed and ended the day at USD 72.08/b. At these levels there is clear room ahead for oil to rally further as there are more supply constraint issues affecting the market than a clear and definable demand risk aside from “trade war”. Intraday highs are the near-term targets to overcome before any more pushes higher and considering the momentum carrying oil prices upward we would expect Brent futures to hold above USD 80/b for some time. The Brent forward curve is also taking part in the current exuberance with the 1-2 month spread nearing USD 0.7/b.