Recent Search

Popular Searches

US and Chinese policy makers made progress on trade talks with announcement of a joint statement that stipulates China agreeing to reduce its trade surplus with the US by way of significantly increasing its purchase of US agriculture and energy products. Both sides have agreed to stop imposing new tariffs on each other. In 2017, US imports from China were circa $505 billion vs exports of only $105 billion which lead to China gaining surplus of $350 billion. US expects China to reduce the surplus by $200 billion by 2020 which to us appears ambitious. However, the halting of the trade war and conciliatory tone of discussions is certainly positive for the global trade and global growth.

Despite the ongoing friction between its two major trading partners, US and China, Japan reported pick up in trade activity in April. Exports increased by 7.8% against 5.9% increase in imports and yielded a trade surplus of JPY 626 billion vs expectations of surplus of only JPY 440 billion. Notwithstanding the trade surplus, Japan reported slowing of inflation in April with CPI ex food coming in at an annualised 0.7% -- not even halfway to the Bank of Japan’s 2% target. Prices for energy and mobile phones were the primary factors in the first back-to-back decline in core CPI since April 2016. The problem with low inflation is Japan is that it still largely depends on external factors such as oil prices and the yen’s exchange rate. Services inflation remains largely flat over the longer term. Slowing inflation will likely delay any plans of policy normalisation by the BoJ.

UAE approved changes to rules governing expatriate residency and foreign ownership of companies. The changes, that will allow 100% ownership of businesses by global investors and permit residency visas for investors for as long as 10 years, will take place by the end of this year and are expected to stimulate investment in the country. Part of the circa AED 164 billion that the expats currently remit abroad may stay on onshore and be invested in local assets.

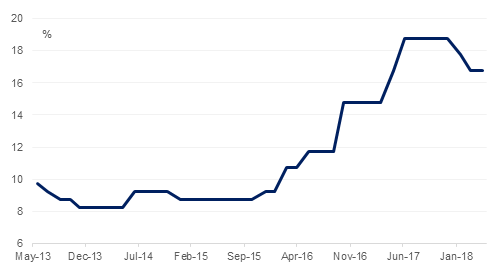

The Central Bank of Egypt kept its benchmark interest rates unchanged on Thursday, as concerns over rising oil prices and upcoming subsidy cuts causing higher inflation trumped the desire to stimulate private consumption. The hold followed two interest rate cuts in February and March which took the overnight lending rate and the overnight deposit rate to 17.75% and 16.75% respectively.

Treasuries closed lower across the board as some key levels were tested. The USTs did pare some of early week losses following gains in 10y bunds amid concern over the new coalition government in Italy. The yield on the 2y UST, 5y UST, 10y UST closed at 2.54% (+1bp w-o-w), 2.88% (+5bps w-o-w) and 3.05% (+9 bps w-o-w). Yield on 10y Italian government bonds rose +36bps w-o-w to 2.22%.

Regional bonds drifted lower as they tracked move in benchmark yields. The YTW on the Bloomberg Barclays GCC Credit and High Yield index closed at 4.68% (+9 bps w-o-w) and credit spreads widened +3bps to 185bps.

Commercial Bank of Qatar raised USD 500mn through a USD bond which was priced at MS+212.5 bps. Qatar National Bank raised USD 1.5bn from a floating rate bond. The formula is set at quarterly US Libor plus 135 bps.

Union Properties has received an approval for issuance of a private sukuk of up to AED 1bn with profit rate not exceeding 9%. The private placement can be to one or more qualified investors with repayment within 10 years. The sukuk will not be convertible into shares.

In terms of rating action, S&P affirmed the A- credit rating of Ruwais Power as the company continues to demonstrate solid operational performance. The outlook is stable.

The dollar index climbed 1.22% during the last five trading days to reach 93.67, a level last seen in December 2017. Technical analysis of the index shows a few key revelations. The index has now broken above the former resistive 50% one year Fibonacci retracement (93.06) which is now acting as a support level. In addition, analysis of the daily candle chart shows that the daily downtrend that has been in effect since March 2017 has now been firmly breached, with 20 consecutive closes above this level.

On the other hand, the weekly candle chart shows that longer-term downtrend has not completely been reversed, and a weekly close above 94.00 needs to be realized in order for a break of this pattern to be achievable. Before this can happen, there needs to be a daily close above 94.20 (the 61.8% one year Fibonacci retracement).

Regional markets closed mixed amid low volumes. The Qatar Exchange dropped -0.4% while the DFM index added +0.2%. In terms of stocks, Jabal Omar rallied +4.8% following an agreement to sell 90 residential units to Albilad Capital for SAR 1.105bn. The impact of the transaction will be seen in Q2 2018 earnings. Drake & Scull continued their positive run from last week with gains of +1.7%.

Oil prices managed to extend their rally last week with Brent futures gaining six weeks in a row. Brent gained 1.8% on the week, closing at USD 78.51/b and did manage to break as high as USD 80.50/b. WTI added 0.8% over the week to close at USD 71.28/b. The US drilling rig count held steady last week at 844, up 124 from the same time a year ago.