Recent Search

Popular Searches

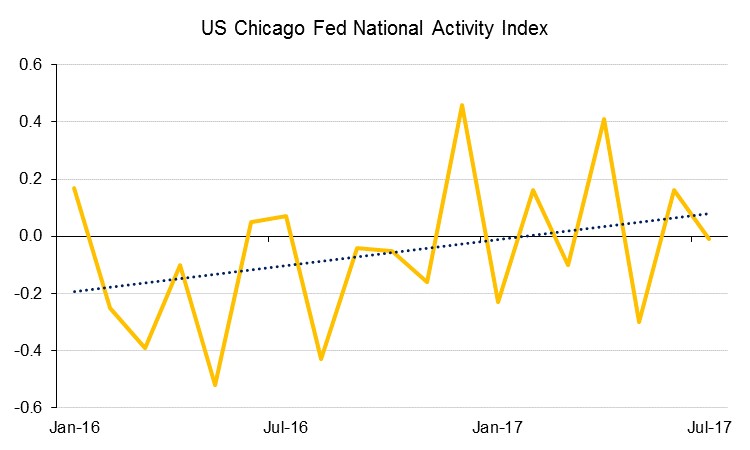

The global economic calendar is a particularly sparse one at the start of this week, with the US Chicago Fed National Activity index the only economic indicator released yesterday. This is not a particularly widely followed index but it showed a slight decline in overall activity to -0.01 in July after a positive reading of +0.16 in June. Of the 85 indicators that make up the index, 42 made positive contributions. Despite this dip in activity the trend in this index is still an improving one (see chart below). However, investors are waiting for the more significant data points later in the week (such as US Durable goods orders on Friday) as well as Fed Chair Yellen’s speech at the Jackson Hole central bank symposium.

Following last week’s upward revision to Q2 Eurozone GDP to 2.2% y/y, markets will turn their attention today to the German ZEW survey for August to see if economic recovery is being sustained in the Eurozone’s largest economy into Q3. The consensus among 27 forecasters polled by Bloomberg is for the ZEW Germany Assessment of Current Situation to drop back to 85.2 in August from 86.4 in July, with the expectations component also thought likely to have eased a little to 15.5 from 17.5 previously. In particular, it is expected that the recent appreciation of the Euro combined with heightened geopolitical uncertainty will have weighed on sentiment, something that markets are wondering whether the ECB will reflect in their upcoming decisions. The ECB Council is not meeting this month, but its President Mario Draghi will be speaking later this week and may touch on issues related to monetary policy normalization, although he is unlikely to focus in detail on the specific issues of the Eurozone economy.

The only other economic data today will be from the UK where public finance figures for July are released and expected to show that government borrowing dipped a little during the month.

Source: EIKON, Emirates NBD Research

Source: EIKON, Emirates NBD Research

|

| Time | Cons |

| Time | Cons |

| UK Public finances | 12.30 | N/A | US FHFA House Prices | 17:00 | 0.50% |

| ZEW Surveys | 13:00 | N/A | Richmond Fed Index | 18:00 | 10.0 |

Source: Bloomberg.

Treasuries continued to hold onto their gains from last week even as they traded in a tight range. Yields on the entire curve was lower by 1-2 bps with 2y USTs yielding 1.30%, 5yUSTs 1.75% and 10y USTs 2.18%.

Regionally, bonds continue to remain in a tight range. Yield on the Bloomberg Barclays GCC and High Yield index rose 1 bps to 3.47% while credit spreads widened 2 bps to 169.

Saudi Arabia issued the second tranche of local currency sukuk and raised SAR 13bn. The issue received offers exceeding SAR 38bn. The government has now raised SAR 30bn so far in 2017.

In terms of rating action, Fitch affirmed Ras Al Khaimah at A and maintained stable outlook. The rating agency said that the ratings reflect the benefits of RAK’s membership of the UAE and a low government debt burden.

Limited activity in FX overnight with geopolitical and economic news both much calmer than of late, allowing USDJPY to sneak higher. However, it is worth keeping an eye on the Korean peninsula, with Pyongyang yesterday warning of a ‘merciless strike’ as the US and South Korea prepare for military drills over the next two weeks. The EUR is also firmer approaching the Jackson Hole meetings as the markets are on guard in case ECB President Draghi sets the stage for QE tapering in coming months, although failure to address the issue may see it give back ground next week.

It was a mixed session of trading for developed market equities with the S&P 500 index adding +0.1% and the Euro Stoxx 600 index dropping -0.4%. The lingering impact of last week’s price action and absence of active money was visible in yesterday’s trading session.

Regional equities closed mixed with the DFM index losing -0.6% and the Tadawul adding +0.2%. There is no catalyst for broad price action and hence market moves are mainly flow driven.

REITs in Saudi Arabia rallied ahead of the listing of Maather REIT. In fact, all four listed REITs were among the most traded stocks with Al Jazira Mawten REIT rallying as much as +9.6%.

Oil prices started the week on the back foot with both Brent and WTI futures giving up more than 2%. Brent futures are now back to a USD 51/b handle while WTI is below USD 48/b. There were few fundamental catalysts to cause prices to dip so significantly. Kuwait's oil minister even suggested that OPEC would discuss extending their current production cut at their upcoming meeting in November. Despite the drop at the front end of the curve, Brent remains in a very tentative backwardation and the rest of the curve is exceptionally flat.

Metals continued their upward move with all the LME complex aside from lead moving higher. Precious metals all edged higher as well on the back of a softer USD.