Recent Search

Popular Searches

.jpg?la=en&h=457&w=800&hash=B26CD4A8776BE2EA4ECE240BB1DFF931)

EM central banks moved to get ahead of the game at the end of last week, with the Turkish and Russian central banks both raising interest rates, in Turkey’s case quite aggressively by 625bps to 24%. Both moves served to put a floor under their respective currencies, which is just as well as US data released on Thursday and Friday maintained the likelihood of a rate hike from the Fed at the end of this month which will likely keep the USD bid adding to pressure on EM FX.

Trade tensions also continue to increase, with the Trump White House sending mixed signals to China, on the one hand inviting Chinese officials back to talks while on the other President Trump indicated that tariffs on USD200bn of Chinese goods would still go ahead. China’s CNY remains vulnerable on the back of these developments with USDCNY pushing back up to wards 6.88 last week. With the latest round of monthly economic activity indicators from China scheduled for the end of the week, these will become increasingly important to monitor as its economy is highly correlated to global trade flows, especially with the China market being an important export destination for many of other EM economies. Some are hopeful that the trade dispute between the US and China will be resolved by the US mid-term Congressional elections on November 6th, but this remains too optimistic in our view with a greater danger that trade war risks extend beyond this date and spread to take in the EU and Japan.

In the coming week the Bank of Japan is widely expected to leave its short term interest rate target unchanged at -0.1% this week and to maintain its policy of yield curve control. The Swiss National Bank is also widely expected to maintain its deposit rate at -0.75% and the range for 3-month Libor held at -1.25% to -0.25%. Meanwhile the economic data flow in the US will be quiet with only US housing starts of any note ahead of the FOMC meeting on the 26th November. Finally EU leaders are scheduled to discuss progress over Brexit at a summit in Salzburg on Thursday, and following encouraging comments from EU Brexit negotiator Barnier and from UK officials, the EU is expected to agree to hold an extraordinary meeting in November to sign off on a deal on future relations.

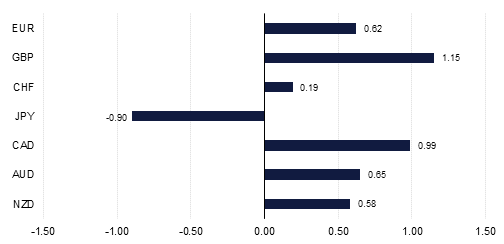

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg