Recent Search

Popular Searches

Weekend violence in Spain’s Catalonia region over an unofficial referendum for independence is making the headlines this morning causing the EUR to struggle. Catalan separatist leaders may declare independence later this week as a result of the vote, which saw 2 million out of 5 million eligible voters support independence although it is unclear what legal basis such a declaration would have. However, it would put the Spanish government and the EU in a quandary about how to react, with the attempt to suppress the referendum playing into the opposition hands by threatening to extend the uncertainty and raising doubts about the authority of the national government. The main focus this week will be US jobs data at the end of the week, although these are likely to have been impacted by Hurricanes Harvey and Irma and may not give a clear picture about growth. Expectations of a US rate hike before the end of the year have risen to 70%, although inflation remains subdued as shown by the dip in the underlying core PCE deflator to 1.3% in August.

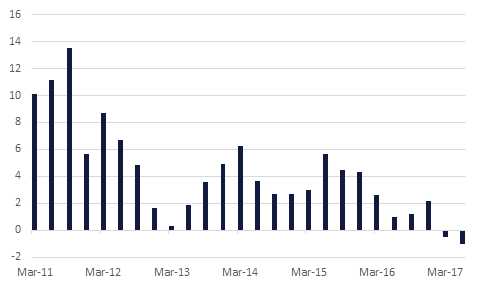

Saudi GDP contracted -1.0% y/y in Q2 2017, down from -0.5% y/y in Q1 2017 and +0.9% y/y in Q2 2016. The main driver was a -2.4% decline in oil sector GDP, which was expected given Saudi Arabia’s compliance with the OPEC production cuts agreed in November 2016. Of greater interest is the acceleration in non-oil GDP in Q2 2017, which reached 0.8% y/y up from 0.5% in Q1. Financial services grew 1.9% y/y last quarter while manufacturing and utilities expanded 1.6% y/y and 1.1% y/y respectively. We expect non-oil growth to gain momentum in H2 2017.

Kuwait has been added to the FTSE Russell Emerging Market Index, which could trigger inflows estimated between USD 600-800mn to Kuwait’s equity market. Kuwait is expected to account for 0.5% of the index. Saudi Arabia was not included in the index on Friday, but will be assessed again in March 2018.

Source: Emirates NBD Research

Source: Emirates NBD Research

Hawkish comments from Federal Reserve Chair, Janet Yellen and supportive economic data out of the US shifted the yield curve on US treasuries upwards with 2yr and 10yr UST yields closing the week at 1.48% (+6bps) and 2.33% (+11bps) respectively. Central banks from the Euro Zone and the UK also appear to be committed to halting their easing bias. Yields on 10yr Gilts and Bunds rose in tandem with USTs, closing the week at 1.36% (+3bps) and 0.46% (+6bps) respectively.

Regional GCC bonds suffered from increasing expectations of a rate hike in the US. Average yield on Barclays GCC bond index rose 6bps to 3.37% even though average credit spreads were narrower by 5bps to 133bps. Shorter dated bonds, including the perpetuals which mostly have call dates between 2018 and 2020, were the main losers. Yields on perpetual securities from FAB, ADIB, GMSEDU, DIB MAF etc widened between 15 to 20bps during the week. That said, high yield bonds such as DARALA, TPZMAR, BHRAIN curve etc outperformed their investment grade counterparts. On the positive front, Dubai Aerospace continued to be well sought by local investors with yield on DUBAEE 22s tightening another 10bps to 4.22% during the week.

The dollar index appreciated last week, broking and closing above the resistive cap of the daily decline that that has been in effect since April 10 2017. Furthermore, supporting that this may be the beginning of a reversal in the trend, the index was able to sustain they break of its 50 day moving average (92.878) and close above this key level for the first time since April. Presently sitting at 93.076, while the index stays above this level, we expect further upside with the 23.6% one year Fibonacci retracement of 94.034 being the next hurdle.

Last week's 1.14% decline took the EURUSD below the 50 day moving average (1.1843) and to consecutive daily closes below the supporting baseline of the former daily uptrend. This is the first time that this has happened since April 2017. Further losses in EURSD were only abated when strong support was found at 1.1717, close to the 200 week moving average (1.1722). Should a sustained break of this level materialise in the coming week, it will catalyse a far greater decline.

It was a mixed start to the week for regional equities. The Tadawul declined -0.7% after FTSE decided to delay including the index in its secondary emerging market index. The decline was led by market heavyweights with Sabic losing -1.0% and Samba dropping -1.3%.

FTSE also decided that the KWSE index would enter the emerging market index in September 2018. This boosted the index heavyweights with Agility adding +1.2% and National Bank of Kuwait gaining +3.3%.

Oil markets spent most of last week paying for Monday’s exuberance. Despite encroaching on USD 60/b Brent futures ended the week up only 1.2%, closing Friday at less than USD 57/b while WTI added nearly 2% on the week to close at USD 51.67/b. Nevertheless, Brent ended the quarter higher, with the quarterly average up 2.6% on Q2 while WTI was nearer to flat.

Market structures closed generally intact, if a little less toppy than they began last week. The backwardation at the front of the Brent curve ended the week at USD 0.20/b for Nov/Dec 2017 while Dec spreads also compressed across 17-18 and 17-19. WTI remains in contango at the front of the curve; Oct-Nov spread closed the week at USD 0.28/b while a muted backwardation is in place from the end of Q1 2018.

Reuters’ estimate of September OPEC production rose 50k b/d to 32.86m b/d thanks to sizeable gains from Saudi Arabia, Iraq, Iraq and Libya. Overall compliance among those party to the production cut agreement slipped to less than 86% as Iraq, Algeria and the UAE fell notably short.