Recent Search

Popular Searches

The Bank of England voted to keep rates on hold at its last MPC meeting although it did temper its expectations for growth on weak performance in the global economy and persistent uncertainty over Brexit. Of note at this decision was that two voters dissented from consensus, both of whom voted for cutting rates by 25bps. The MPC noted that risks related to Brexit remain on the downside and has effectively set a high bar for rates to move upward. Inflation expectations, which had been one of the main points supporting a higher rate outlook in the UK, are now lower out to 2021. Sterling and UK assets remain highly levered to the outcome of the UK’s general election, in which the ruling Conservatives are still leading polls, and how and when Brexit gets delivered. Elsewhere, Moody’s placed the UK’s sovereign rating on a negative outlook citing the country’s current policy paralysis.

The European Commission cut its growth forecasts for 2019 and 2020, expecting GDP growth of just 1.1% this year and 1.2% next year. Weak performance in the industrial sectors of core economies, as reflected by still struggling PMIs, has been weighing on growth. Industy data will be released mid-week with expectation that it will show more declines in place while later in the week markets will focus on whether Germany managed to avoid a recession in Q3 when GDP data are released.

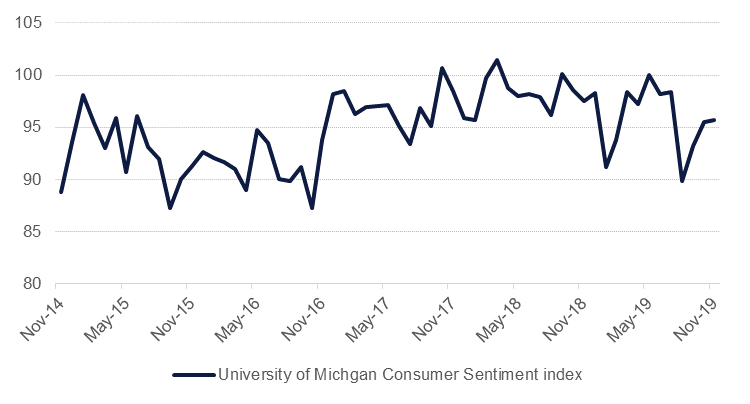

The University of Michigan’s consumer sentiment survey gained a third month running, hitting 95.7 and beating market expectations. The assessment of future expectations moved to a fourth-month high while sentiment toward individuals’ financial situation improved. Meanwhile, New York Fed president John Williams said he believed that the US economy was in a “good place” after adjustments to rates and that current interest rates were supportive for growth.

Egypt’s headline CPI inflation rate fell to a more-than-nine-year low of 3.1% in October, down from 4.8% the previous month. The ongoing disinflation has taken real interest rates to 10.15% at current levels, lending upside risk to our expectation of a 100bps cut at the Central Bank of Egypt’s MPC meeting on Thursday – we now see scope for a 150bps cut reduction to the benchmark overnight deposit rate, with a further cut likely in December. Lower rates will substantially reduce the government’s cost of servicing debt, much of which is held in domestic papers.

Source: Emirates NBD Research

Source: Emirates NBD Research

Fixed Income

Treasuries closed sharply lower as risk appetite gathered pace following better than expected economic data and positive news flow around Phase 1 trade deal between the US and China. The curve steepened with yields on the 2y UST, 5y UST and 10y UST closing at 1.67% (+12 bps w-o-w), 1.74% (+20 bps w-o-w) and 1.94% (+23 bps w-o-w) respectively.

Following the moves in yields, the scheduled testimony of the Fed Chair Jerome Powell before the US Congress will be keenly watched.

In emerging market space, Moody’s cut India’s credit rating outlook to negative. The rating agency cited worsening shadow banking crunch, prolonged slowdown in economy and a rising public debt as reasons. The rating was retained at Baa2. Yields on the 10y government bonds rose +11bps w-o-w to 6.55%. The move marked a reversal of trend wherein yields had dropped for the last three consecutive weeks.

Regional bonds closed lower as they moved out of a tight range. The YTW on Bloomberg Barclays GCC Credit and High Yield index rose +6 bps w-o-w to 3.33% and credit spreads tightened 12 bps w-o-w to 148 bps.

Notwithstanding a slight pause in secondary markets gains, primary markets continue to see some interest. Dubai Islamic Bank mandated banks for a possible sukuk issuance.

The USD and JPY recovered a little on Friday as President Trump indicated that he had not decided to roll-back tariffs on China as part of a trade deal between the two countries. The USD made gains against most major currencies, with the JPY the only slight exception. USDJPY slipped to 109.18 while EURUSD touched trend lows of 1.1017. The USD was also stronger over the week as a whole. GBP softened slightly as markets eyed opinion polls, but with the greater likelihood being either a Conservative government or a hung parliament the downside to sterling is likely to be limited from here.

Regional equities started the new week on a mixed note. Flows were dominated by changes to the MSCI EM index. Arab National Bank gained as the stock was included in the index while Emaar Development dropped -7.2% after the stock was removed from the index. Other Emaar-related names also reacted negatively to the development with Emaar Malls and Emaar Properties losing -0.5% and -1.2% respectively.

Oil markets gained last week on optimism that a trade deal was nearing completion between the US and China. Brent futures closed the week at USD 62.51/b, up 1.3% and more than offsetting the prior week’s decline, while WTI added 1.85% over the week to settle at USD 57.24/b. Oil is weaker to start trading, however, with both Brent and WTI futures down by around 0.7% in early trades.

Saudi Aramco released the prospectus for its IPO although it did not provide substantial details over pricing or the valuation of the company. The prospectus did highlight, though, that production was a Saudi government decision, not Aramco’s, and that the country remains committed to abiding by OPEC decisions over the level of output. This has reaffirmed our view that the IPO itself does not affection production decisions in the short-term.

Edward Bell

Edward Bell