Recent Search

Popular Searches

Source: Emirates NBD Research

Source: Emirates NBD Research

Fixed Income

Treasury yields moved higher yesterday as markets turned to a risk-on posture following a deal US president Trump made with Democrats regarding the debt ceiling. The Treasury will get a three month extension until December to continue financing the government. Yields on 10yr USTs closed above 2.1%, gaining nearly 4bps. The 2-10 spread held relatively steady yesterday while the inversion in the TBill end of the curve reversed back to normal conditions.

GCC local bonds were well bid in the face of stable oil prices and absence of new supply. Credit spreads on Bloomberg Barclays GCC index tightened 5bps to 143bps, leading to a 2bp tightening in average yield to 3.24% yesterday. That said, CDS levels on GCC sovereigns closed range bound with slight widening bias. 5yr CDS on Saudi and Qatar were largely unchanged at 86bps and 92bps respectively.

In the primary market, Bahrain has mandated banks for possible 7yr, 12yr and 30yr sukuk tranches.

FX

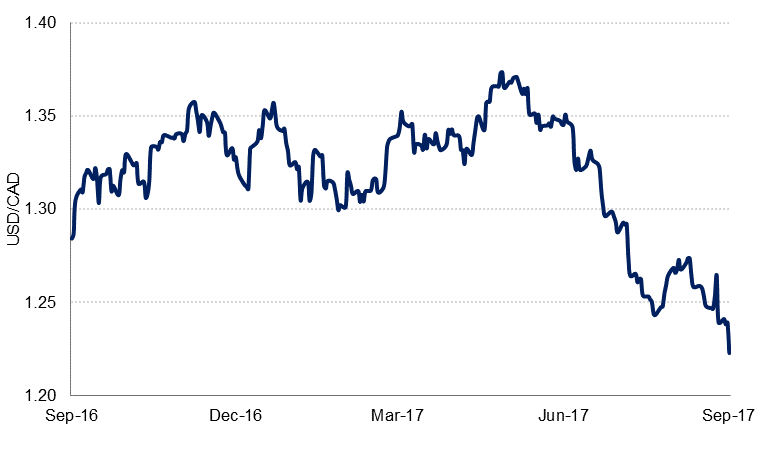

The biggest mover overnight was unsurprisingly CAD, following the surprise 25bp rate hike yesterday. CAD is now at the strongest level since mid-2015. The BoC’s statement was relatively cautious, and while it did not specifically mention the exchange rate as a risk factor, it did cite unspecified “financial market developments” as a potential risk going forward. Over the course of the day USDCAD declined 1.2% to 1.2226, having hit lows of 1.2146 in the immediate aftermath of the rate announcement. The move reaffirms the daily downtrend that we have seen in effect since 5th May 2017 and broke through the previous 0% one year Fibonacci retracement, so set new lows. Another break and close below the 50% five year Fibonacci retracement (1.2161) exposes a potential risk of further declines towards 1.1565, the 38.2% five year Fibonacci retracement.

Equities

US equity markets managed to close higher on the day—the S&P rose 0.3%--as enthusiasm for risk assets returned. European equity markets also ended the day higher ahead of the ECB meeting today where some confident statements about the regional economy are to be expected. Regional performance was scatter shot: the Tadawul closed up 0.7% while the ADX and DFM lost and gained 0.5% respectively.

Commodities

Oil markets continued to move higher yesterday as refinery demand is expected to pick up and the Gulf of Mexico braces for the new impact of Hurricane Irma, which may affect production more acutely than Harvey had. Weekly EIA data will be delayed owing to the Labor Day holiday in the US at the start of the week.

Brent prices closed up 1.5% and WTI futures around 1%. The front of the WTI curve is still holding in a reasonably wide contango of over USD 0.4/b while the front of the Brent curve is just above USD 0.15/b in backwardation. December spreads for both benchmarks remain in contango.

OPEC exports reportedly fell in August to their lowest level since April according to an assessment by Reuters. However, on average exports in the first eight months of the year have been higher than the same period last year despite OPEC’s efforts to force a rebalancing but cutting down on global inventories.